Diamond Hill Investment Group Inc. Files Definitive Proxy Statement

Ticker: DHIL · Form: DEF 14A · Filed: Mar 25, 2024 · CIK: 909108

| Field | Detail |

|---|---|

| Company | Diamond Hill Investment Group Inc (DHIL) |

| Form Type | DEF 14A |

| Filed Date | Mar 25, 2024 |

| Risk Level | low |

| Pages | 16 |

| Reading Time | 19 min |

| Key Dollar Amounts | $3 billion, $3.9 billion, $29.2 b, $27.3 b, $1.4 billion |

| Sentiment | neutral |

Sentiment: neutral

Topics: DEF 14A, Proxy Statement, Executive Compensation, Equity Awards, Corporate Governance

TL;DR

<b>Diamond Hill Investment Group Inc. filed its DEF 14A proxy statement for the fiscal year ending December 31, 2023, detailing executive compensation and equity awards.</b>

AI Summary

DIAMOND HILL INVESTMENT GROUP INC (DHIL) filed a Proxy Statement (DEF 14A) with the SEC on March 25, 2024. Diamond Hill Investment Group Inc. filed a Definitive Proxy Statement (DEF 14A) on March 25, 2024. The filing covers the fiscal year ending December 31, 2023. The company's principal executive offices are located at 325 John H. McConnell Blvd, Suite 200, Columbus, OH 43215. The filing includes data related to equity awards granted to PEO and Non-PEO members for the years 2020 through 2023. Diamond Hill Investment Group Inc. was formerly known as Banc Stock Group Inc., Heartland Group of Companies Inc., and Heartland Financial Group Inc.

Why It Matters

For investors and stakeholders tracking DIAMOND HILL INVESTMENT GROUP INC, this filing contains several important signals. This DEF 14A filing provides shareholders with crucial information regarding executive compensation, stock awards, and other governance matters, enabling informed voting decisions. The detailed breakdown of equity awards granted to both executive and non-executive personnel over several years offers insight into the company's long-term incentive strategies and potential dilution effects.

Risk Assessment

Risk Level: low — DIAMOND HILL INVESTMENT GROUP INC shows low risk based on this filing. The filing is a routine DEF 14A, indicating standard corporate governance procedures rather than immediate financial distress or significant operational changes.

Analyst Insight

Review the executive compensation details and equity award grants to understand potential impacts on shareholder value and dilution.

Key Numbers

- 2023-12-31 — Fiscal Year End (Period of Report)

- 2024-03-25 — Filing Date (Date Filed)

- 1934 Act — SEC Act (Governing Act)

- 000-24498 — SEC File Number (SEC Filing Identifier)

Key Players & Entities

- DIAMOND HILL INVESTMENT GROUP INC (company) — Filer

- 325 JOHN H MCCONNELL BLVD (address) — Business Address

- COLUMBUS (location) — Business Address City

- OH (location) — Business Address State

- BANC STOCK GROUP INC (company) — Former Company Name

- HEARTLAND GROUP OF COMPANIES INC (company) — Former Company Name

- HEARTLAND FINANCIAL GROUP INC (company) — Former Company Name

FAQ

When did DIAMOND HILL INVESTMENT GROUP INC file this DEF 14A?

DIAMOND HILL INVESTMENT GROUP INC filed this Proxy Statement (DEF 14A) with the SEC on March 25, 2024.

What is a DEF 14A filing?

A DEF 14A is a definitive proxy statement sent to shareholders before annual meetings, covering executive compensation, board nominations, and shareholder votes. This particular DEF 14A was filed by DIAMOND HILL INVESTMENT GROUP INC (DHIL).

Where can I read the original DEF 14A filing from DIAMOND HILL INVESTMENT GROUP INC?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by DIAMOND HILL INVESTMENT GROUP INC.

What are the key takeaways from DIAMOND HILL INVESTMENT GROUP INC's DEF 14A?

DIAMOND HILL INVESTMENT GROUP INC filed this DEF 14A on March 25, 2024. Key takeaways: Diamond Hill Investment Group Inc. filed a Definitive Proxy Statement (DEF 14A) on March 25, 2024.. The filing covers the fiscal year ending December 31, 2023.. The company's principal executive offices are located at 325 John H. McConnell Blvd, Suite 200, Columbus, OH 43215..

Is DIAMOND HILL INVESTMENT GROUP INC a risky investment based on this filing?

Based on this DEF 14A, DIAMOND HILL INVESTMENT GROUP INC presents a relatively low-risk profile. The filing is a routine DEF 14A, indicating standard corporate governance procedures rather than immediate financial distress or significant operational changes.

What should investors do after reading DIAMOND HILL INVESTMENT GROUP INC's DEF 14A?

Review the executive compensation details and equity award grants to understand potential impacts on shareholder value and dilution. The overall sentiment from this filing is neutral.

How does DIAMOND HILL INVESTMENT GROUP INC compare to its industry peers?

Diamond Hill Investment Group Inc. operates in the investment advice industry, providing asset management services.

Are there regulatory concerns for DIAMOND HILL INVESTMENT GROUP INC?

The filing is made under the Securities Exchange Act of 1934, requiring public companies to disclose information to shareholders.

Industry Context

Diamond Hill Investment Group Inc. operates in the investment advice industry, providing asset management services.

Regulatory Implications

The filing is made under the Securities Exchange Act of 1934, requiring public companies to disclose information to shareholders.

What Investors Should Do

- Analyze the executive compensation structure and any proposed changes.

- Evaluate the details of equity awards granted, including vesting schedules and potential dilution.

- Review any shareholder proposals or director nominations presented in the proxy statement.

Key Dates

- 2024-03-25: Filing Date — Definitive Proxy Statement (DEF 14A) filed.

- 2023-12-31: Fiscal Year End — Reporting period for the proxy statement.

Year-Over-Year Comparison

This is the initial filing analyzed for the current period, so no direct comparison to a prior filing is available within this data.

Filing Stats: 4,670 words · 19 min read · ~16 pages · Grade level 12.6 · Accepted 2024-03-25 09:41:43

Key Financial Figures

- $3 billion — r fixed income strategies surpassed the $3 billion mark. As of 29 February 2024, our fixed

- $3.9 billion — 2024, our fixed income assets exceeded $3.9 billion. We have made significant investments t

- $29.2 b — M) and assets under advisement (AUA) of $29.2 billion, our average during the year was

- $27.3 b — illion, our average during the year was $27.3 billion, down 8% from 2022. Additionally,

- $1.4 billion — , partly due to fixed income inflows of $1.4 billion and equity outflows of $1.9 billion. Fi

- $1.9 billion — of $1.4 billion and equity outflows of $1.9 billion. Fixed income assets, which typically h

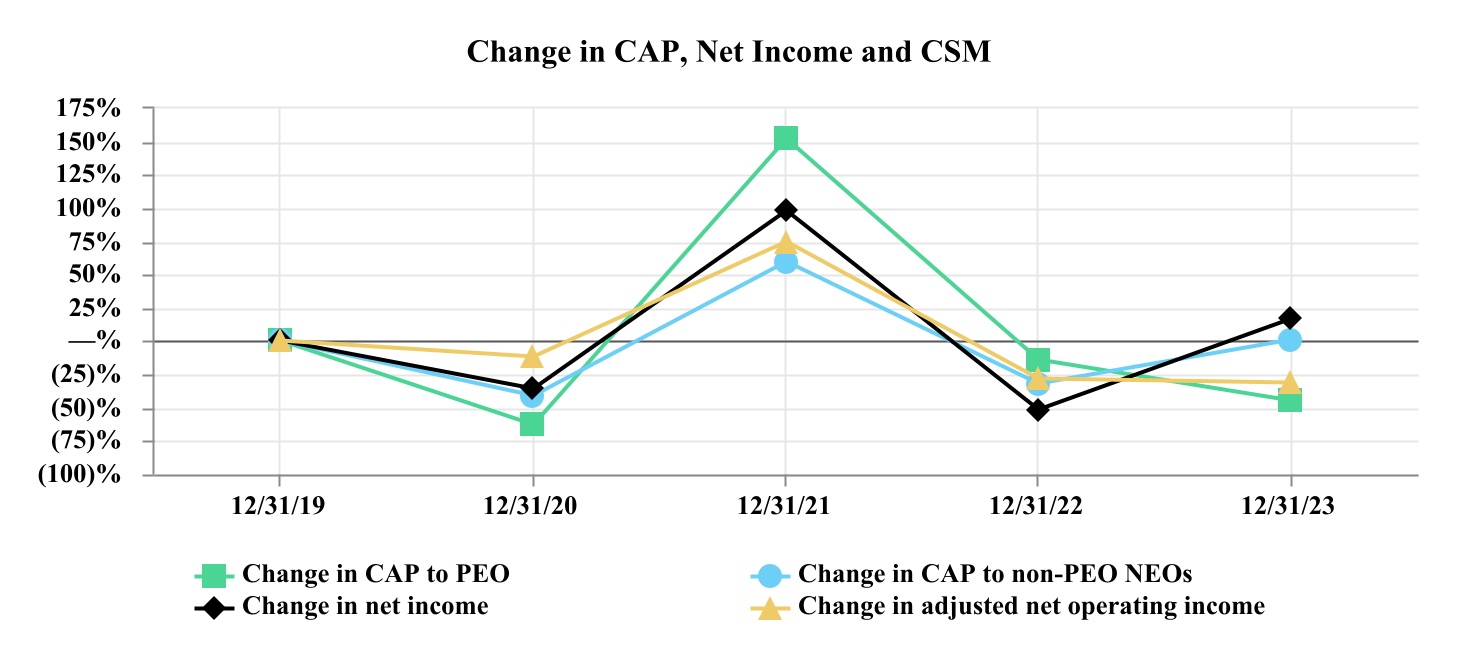

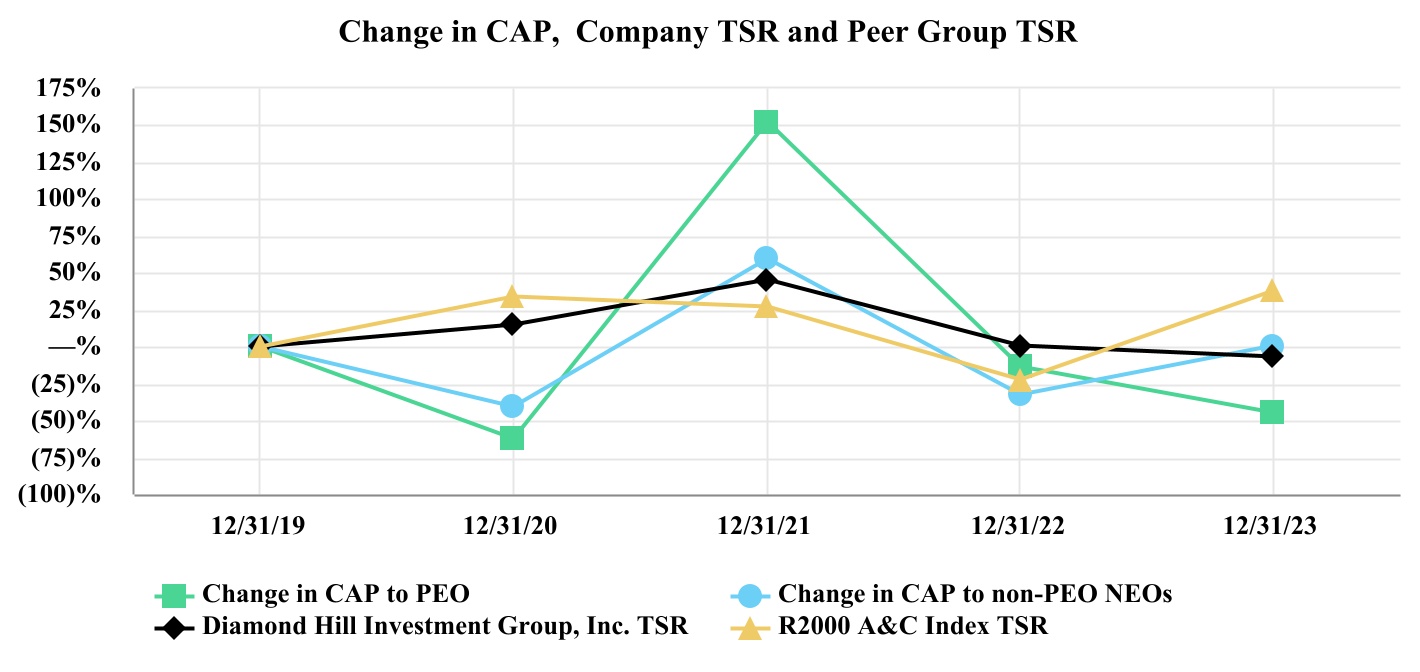

- $35.5 million — 3. We generated net operating income of $35.5 million and net operating profit margin of 26%

- $41.4 million — date. Adjusted net operating income was $41.4 million in 2023, down from $60.4 million in 202

- $60.4 million — me was $41.4 million in 2023, down from $60.4 million in 2022, and our adjusted net operating

- $29 b — ly boosted our ending AUM and AUA above $29 billion, more than $2.5 billion higher th

- $2.5 billion — UM and AUA above $29 billion, more than $2.5 billion higher than where we started the year.

- $23 million — ly, the strong market returns generated $23 million in investment 1 Adjusted net operatin

- $42.2 m — attributable to common shareholders was $42.2 million, up from $40.4 million in 2022, a

- $40.4 million — shareholders was $42.2 million, up from $40.4 million in 2022, and our earnings per share inc

- $14.32 — and our earnings per share increased to $14.32 from $13.01 in the prior year. Capita

Filing Documents

- dhil-20240325.htm (DEF 14A) — 787KB

- dhil-20240325_g1.jpg (GRAPHIC) — 602KB

- dhil-20240325_g2.jpg (GRAPHIC) — 43KB

- dhil-20240325_g3.jpg (GRAPHIC) — 6KB

- dhil-20240325_g4.jpg (GRAPHIC) — 149KB

- dhil-20240325_g5.jpg (GRAPHIC) — 156KB

- dhil-20240325_g6.jpg (GRAPHIC) — 79KB

- dhil-20240325_g7.jpg (GRAPHIC) — 320KB

- 0000909108-24-000012.txt ( ) — 4628KB

- dhil-20240325.xsd (EX-101.SCH) — 3KB

- dhil-20240325_def.xml (EX-101.DEF) — 5KB

- dhil-20240325_lab.xml (EX-101.LAB) — 6KB

- dhil-20240325_pre.xml (EX-101.PRE) — 4KB

- dhil-20240325_htm.xml (XML) — 160KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

From the Filing

dhil-20240325 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A INFORMATION Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 Filed by the Registrant x Filed by a Party other than the Registrant Check the appropriate box: Preliminary Proxy Statement Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) x Definitive Proxy Statement Definitive Additional Materials Soliciting Material under 240.14a-12 DIAMOND HILL INVESTMENT GROUP, INC. (Name of registrant as specified in its charter) (Name of person(s) filing proxy statement, if other than the registrant) Payment of Filing Fee (Check all boxes that apply): x No fee required Fee paid previously with preliminary materials. Fee computed on table in exhibit required by Item 25(b) per Securities Exchange Act Rules 14a-6(i)(1) and 0-11. 1 DIAMOND HILL INVESTMENT GROUP, INC. ANNUAL LETTER TO SHAREHOLDERS March 25, 2024 Dear Fellow Shareholders: At Diamond Hill, we are fiercely committed to improving the lives of our clients and those they serve through the pursuit of exceptional investment results. Doing so requires discipline, patience, and a passion for what we do and who we serve. That passion drives us to develop outstanding, long-term partnerships with our clients because we know that excellent investment outcomes enable them to achieve their goals. Achieving our long-term goals in an industry where change is constant can be challenging, especially when active managers continue to face several significant industry headwinds. Passive has been on the rise for decades — as of year-end 2023, assets in passive funds and ETFs surpassed their active counterparts. Against this backdrop, new funds launched have struggled to gain traction with only a small number reaching scale within five years. Pairing this trend with increased demand for private assets in the institutional space and increasingly in retail, traditional active managers continue to be squeezed from both sides. And, of course, costs have been rising for asset managers — including distribution costs, growing product suites and the related data and technology to support them, operational and IT costs, and the ability to retain top investment talent to deliver strong results for clients. At the same time, rising revenues over the last 15 years have enabled a lack of cost discipline to persist within the industry. With revenues now slowing, the industry is starting to see the implications of higher cost structures. As we look ahead, we understand the headwinds in front of us, and given our competitive advantages and our discipline to stay focused, we believe we are positioned well for long-term success. To succeed in this challenging environment over the long term, we must take market share from our competitors by delivering long-term outperformance and an exceptional client experience that differentiates us. On balance, investors are allocating more to passive products as well as to private equities and credit. Many of our competitors have pursued aggressive acquisition strategies to shift their businesses to meet that demand. The reality is that publicly traded active equity and fixed income are enormous categories that aren't going anywhere anytime soon. In our view, this environment presents opportunities for those focused on actively managing concentrated portfolios with a valuation discipline and long-term ownership mindset. As such, we remain committed to our investment philosophy and approach, and we believe we can continue to deliver highly competitive investment outcomes for our clients. It's important to remember investors in passive products face higher investment risks than ever before. A handful of companies are now dominating US equity markets, exacerbating the already highly concentrated nature of returns. The tech-centric Magnificent 7 — Apple, Microsoft, Amazon, Alphabet, Nvidia, Meta and Tesla — accounted for more than half of 2023's returns for index-based products tracking large-cap US equities. Passive strategies, by definition, do not come with the long-term analysis or portfolio oversight of their actively managed counterparts. The winning investments become an even greater share of the index, further tilting toward added risk. Investors have been willing to make that trade-off in strong market environments, and time will tell if this imbalance is sustainable. We are convinced that active management remains an essential component of investors' success in the long run. Instead of pursuing passive or private markets, as always, we remain focused on our strengths and prioritize areas where we have a competitive edge. While we know it will take dedication and resilience to succeed in the active strategies we've built our business on, fewer firms focused on this particular arena should further enable us to continue adding value for our clients and shareh