Federal Home Loan Mortgage Corp. Files 2023 Annual Report

Ticker: FMCKK · Form: 10-K · Filed: Feb 14, 2024 · CIK: 1026214

| Field | Detail |

|---|---|

| Company | Federal Home Loan Mortgage Corp (FMCKK) |

| Form Type | 10-K |

| Filed Date | Feb 14, 2024 |

| Risk Level | medium |

| Pages | 15 |

| Reading Time | 18 min |

| Key Dollar Amounts | $1.00, $10.5 b, $21.2 b, $47.7 billion, $37.0 billion |

| Sentiment | neutral |

Sentiment: neutral

Topics: 10-K, Annual Report, Mortgage Finance, Financials, Federal Home Loan Mortgage Corp

TL;DR

<b>Federal Home Loan Mortgage Corp. has submitted its 2023 annual 10-K report detailing its financial performance and operations.</b>

AI Summary

FEDERAL HOME LOAN MORTGAGE CORP (FMCKK) filed a Annual Report (10-K) with the SEC on February 14, 2024. Federal Home Loan Mortgage Corp. filed its 10-K annual report for the fiscal year ending December 31, 2023. The filing covers the period from January 1, 2023, to December 31, 2023. Key financial data points and stock information are included in the report. The company's principal business address is 8200 Jones Branch Dr, McLean, VA 22102. The filing was made on February 14, 2024.

Why It Matters

For investors and stakeholders tracking FEDERAL HOME LOAN MORTGAGE CORP, this filing contains several important signals. This 10-K filing provides a comprehensive overview of the company's financial health and operational activities for the fiscal year 2023, crucial for investors and stakeholders to assess performance and future outlook. As a federally sponsored entity, the company's filings are closely watched for insights into the broader mortgage market and housing finance sector.

Risk Assessment

Risk Level: medium — FEDERAL HOME LOAN MORTGAGE CORP shows moderate risk based on this filing. The company operates in a highly regulated financial sector, subject to government oversight and policy changes that could impact its business model and profitability.

Analyst Insight

Review the detailed financial statements and risk factors in the 10-K to understand the company's exposure to interest rate fluctuations and regulatory changes.

Key Numbers

- 2023-12-31 — Fiscal Year End (Period of report)

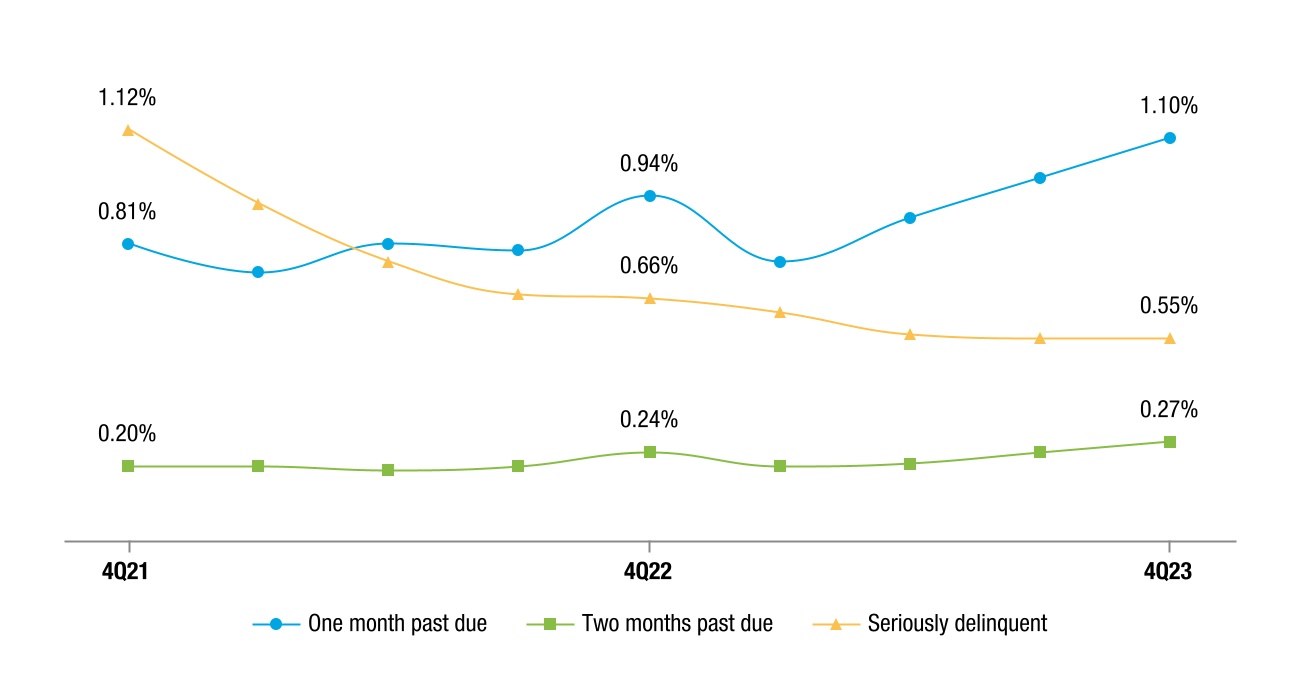

- 2024-02-14 — Filing Date (Date filed)

- 2023-01-01 — Report Start Date (Period of report)

Key Players & Entities

- FEDERAL HOME LOAN MORTGAGE CORP (company) — Filer name

- 8200 JONES BRANCH DR (location) — Business address

- MCLEAN (location) — Business address city

- VA (location) — Business address state

- 22102 (location) — Business address zip

- 1934 Act (regulation) — SEC Act

- 001-34139 (identifier) — SEC file number

FAQ

When did FEDERAL HOME LOAN MORTGAGE CORP file this 10-K?

FEDERAL HOME LOAN MORTGAGE CORP filed this Annual Report (10-K) with the SEC on February 14, 2024.

What is a 10-K filing?

A 10-K is a comprehensive annual financial report required by the SEC, covering audited financials, business operations, risk factors, and management discussion. This particular 10-K was filed by FEDERAL HOME LOAN MORTGAGE CORP (FMCKK).

Where can I read the original 10-K filing from FEDERAL HOME LOAN MORTGAGE CORP?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by FEDERAL HOME LOAN MORTGAGE CORP.

What are the key takeaways from FEDERAL HOME LOAN MORTGAGE CORP's 10-K?

FEDERAL HOME LOAN MORTGAGE CORP filed this 10-K on February 14, 2024. Key takeaways: Federal Home Loan Mortgage Corp. filed its 10-K annual report for the fiscal year ending December 31, 2023.. The filing covers the period from January 1, 2023, to December 31, 2023.. Key financial data points and stock information are included in the report..

Is FEDERAL HOME LOAN MORTGAGE CORP a risky investment based on this filing?

Based on this 10-K, FEDERAL HOME LOAN MORTGAGE CORP presents a moderate-risk profile. The company operates in a highly regulated financial sector, subject to government oversight and policy changes that could impact its business model and profitability.

What should investors do after reading FEDERAL HOME LOAN MORTGAGE CORP's 10-K?

Review the detailed financial statements and risk factors in the 10-K to understand the company's exposure to interest rate fluctuations and regulatory changes. The overall sentiment from this filing is neutral.

How does FEDERAL HOME LOAN MORTGAGE CORP compare to its industry peers?

Federal Home Loan Mortgage Corporation (Freddie Mac) is a government-sponsored enterprise (GSE) chartered by Congress to provide liquidity, stability, and affordability to the U.S. housing market.

Are there regulatory concerns for FEDERAL HOME LOAN MORTGAGE CORP?

As a GSE, Freddie Mac operates under the oversight of the Federal Housing Finance Agency (FHFA) and is subject to specific regulations governing its operations and capital requirements.

Industry Context

Federal Home Loan Mortgage Corporation (Freddie Mac) is a government-sponsored enterprise (GSE) chartered by Congress to provide liquidity, stability, and affordability to the U.S. housing market.

Regulatory Implications

As a GSE, Freddie Mac operates under the oversight of the Federal Housing Finance Agency (FHFA) and is subject to specific regulations governing its operations and capital requirements.

What Investors Should Do

- Analyze the company's financial statements for the fiscal year 2023 to understand revenue streams, expenses, and profitability.

- Review any disclosed risk factors related to interest rate sensitivity, credit risk, and regulatory changes.

- Assess the company's capital structure and liquidity position as detailed in the balance sheet and related notes.

Key Dates

- 2023-12-31: Fiscal Year End — End of the reporting period for the 10-K.

- 2024-02-14: Filing Date — Date the 10-K was officially submitted to the SEC.

Year-Over-Year Comparison

This filing represents the company's annual report for the fiscal year 2023, providing updated financial and operational information compared to previous filings.

Filing Stats: 4,459 words · 18 min read · ~15 pages · Grade level 15.4 · Accepted 2024-02-14 07:54:29

Key Financial Figures

- $1.00 — n-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCI ) 5% Non-Cumul

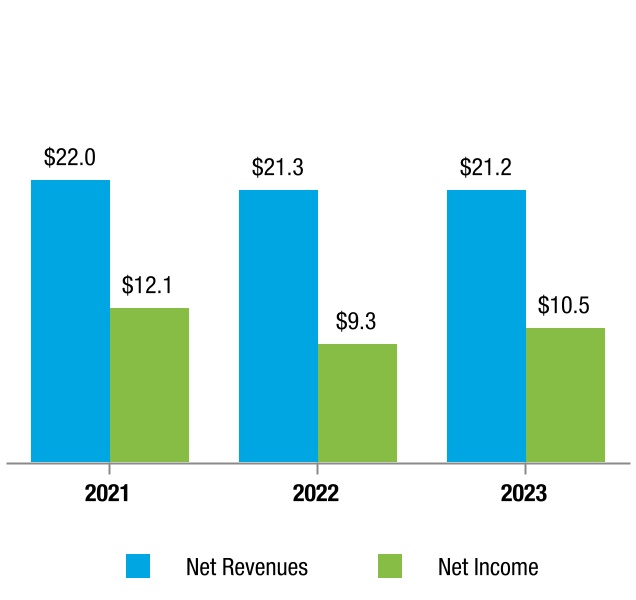

- $10.5 b — ers: n 2023 vs. 2022 l Net income was $10.5 billion, an increase of 13% year-over-yea

- $21.2 b — -interest expense. l Net revenues were $21.2 billion, down slightly year-over-year, as

- $47.7 billion — ion About Freddie Mac l Net worth was $47.7 billion as of December 31, 2023, up from $37.0

- $37.0 billion — illion as of December 31, 2023, up from $37.0 billion as of December 31, 2022. n 2022 vs. 20

- $9.3 b — 022. n 2022 vs. 2021 l Net income was $9.3 billion, a decrease of 23% year-over-year

- $21.3 b — in Single-Family. l Net revenues were $21.3 billion, down 3% year-over-year, as highe

- $28.0 billion — illion as of December 31, 2022, up from $28.0 billion as of December 31, 2021. Market Liqui

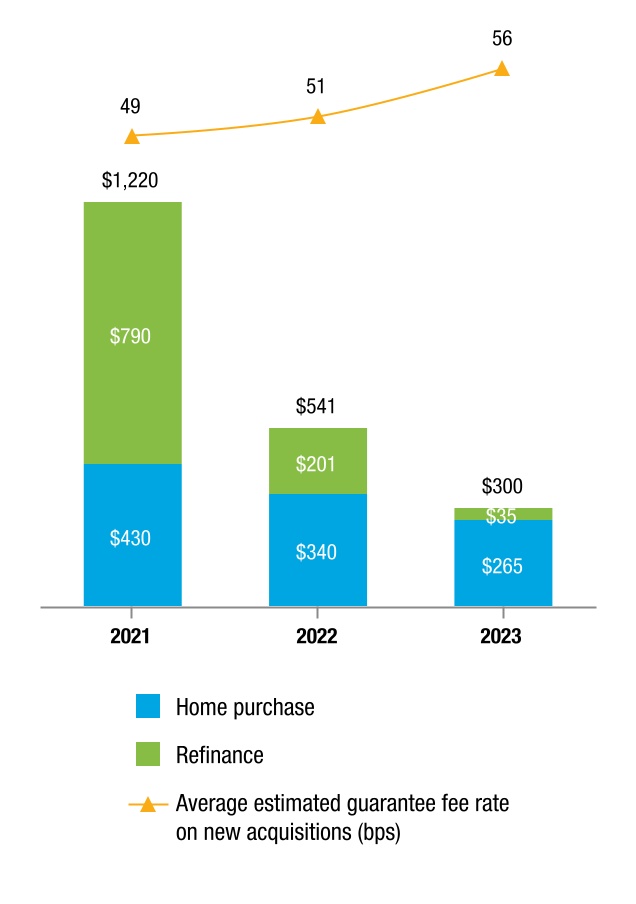

- $348 billion — well as for rental housing. We provided $348 billion in liquidity to the mortgage market in

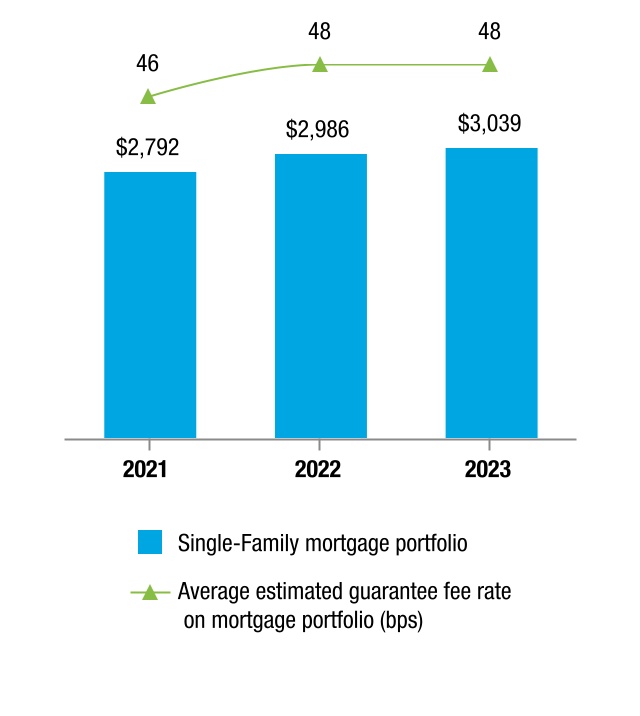

- $3.5 — ortfolio increased 2% year-over-year to $3.5 trillion at December 31, 2023. – Our S

- $3.0 — ur Single-Family mortgage portfolio was $3.0 trillion at December 31, 2023, up 2% ye

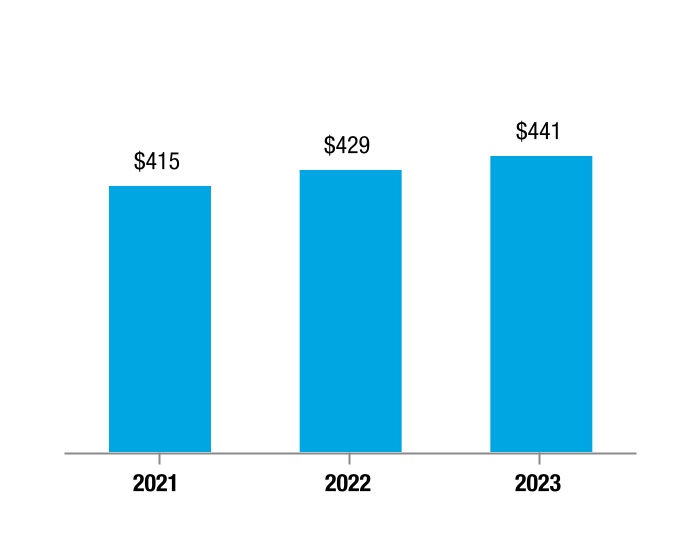

- $441 billion — Our Multifamily mortgage portfolio was $441 billion at December 31, 2023, up 3% year-over-y

- $3.4 — ortfolio increased 6% year-over-year to $3.4 trillion at December 31, 2022. – Our S

- $429 billion — Our Multifamily mortgage portfolio was $429 billion at December 31, 2022, up 3% year-over-y

- $766,550 — a one-family residence has been set at $766,550 for 2024, an increase from $726,200 for

Filing Documents

- fmcc-20231231.htm (10-K) — 7938KB

- a4q2310kexhibit430.htm (EX-4.30) — 101KB

- a4q2310kexhibit1036.htm (EX-10.36) — 38KB

- a4q2310kexhibit1037.htm (EX-10.37) — 8KB

- a4q2310kexhibit241.htm (EX-24.1) — 44KB

- a4q2310kexhibit311.htm (EX-31.1) — 19KB

- a4q2310kexhibit312.htm (EX-31.2) — 19KB

- a4q2310kexhibit321.htm (EX-32.1) — 7KB

- a4q2310kexhibit322.htm (EX-32.2) — 7KB

- fmcc-20231231_g1.jpg (GRAPHIC) — 255KB

- fmcc-20231231_g10.jpg (GRAPHIC) — 2069KB

- fmcc-20231231_g11.jpg (GRAPHIC) — 67KB

- fmcc-20231231_g12.jpg (GRAPHIC) — 45KB

- fmcc-20231231_g13.jpg (GRAPHIC) — 44KB

- fmcc-20231231_g14.jpg (GRAPHIC) — 49KB

- fmcc-20231231_g15.jpg (GRAPHIC) — 70KB

- fmcc-20231231_g16.jpg (GRAPHIC) — 26KB

- fmcc-20231231_g17.jpg (GRAPHIC) — 66KB

- fmcc-20231231_g18.jpg (GRAPHIC) — 54KB

- fmcc-20231231_g19.jpg (GRAPHIC) — 38KB

- fmcc-20231231_g2.jpg (GRAPHIC) — 36KB

- fmcc-20231231_g20.jpg (GRAPHIC) — 35KB

- fmcc-20231231_g21.jpg (GRAPHIC) — 106KB

- fmcc-20231231_g22.jpg (GRAPHIC) — 485KB

- fmcc-20231231_g23.jpg (GRAPHIC) — 553KB

- fmcc-20231231_g24.jpg (GRAPHIC) — 247KB

- fmcc-20231231_g25.jpg (GRAPHIC) — 168KB

- fmcc-20231231_g26.jpg (GRAPHIC) — 133KB

- fmcc-20231231_g27.jpg (GRAPHIC) — 42KB

- fmcc-20231231_g28.jpg (GRAPHIC) — 37KB

- fmcc-20231231_g29.jpg (GRAPHIC) — 53KB

- fmcc-20231231_g3.jpg (GRAPHIC) — 24KB

- fmcc-20231231_g30.jpg (GRAPHIC) — 55KB

- fmcc-20231231_g31.jpg (GRAPHIC) — 49KB

- fmcc-20231231_g32.jpg (GRAPHIC) — 40KB

- fmcc-20231231_g33.jpg (GRAPHIC) — 33KB

- fmcc-20231231_g34.jpg (GRAPHIC) — 32KB

- fmcc-20231231_g35.jpg (GRAPHIC) — 112KB

- fmcc-20231231_g36.jpg (GRAPHIC) — 52KB

- fmcc-20231231_g37.jpg (GRAPHIC) — 54KB

- fmcc-20231231_g38.jpg (GRAPHIC) — 22KB

- fmcc-20231231_g39.jpg (GRAPHIC) — 21KB

- fmcc-20231231_g4.jpg (GRAPHIC) — 62KB

- fmcc-20231231_g40.jpg (GRAPHIC) — 24KB

- fmcc-20231231_g41.jpg (GRAPHIC) — 61KB

- fmcc-20231231_g42.jpg (GRAPHIC) — 24KB

- fmcc-20231231_g43.jpg (GRAPHIC) — 20KB

- fmcc-20231231_g44.jpg (GRAPHIC) — 760KB

- fmcc-20231231_g45.jpg (GRAPHIC) — 20KB

- fmcc-20231231_g46.jpg (GRAPHIC) — 21KB

- fmcc-20231231_g47.jpg (GRAPHIC) — 70KB

- fmcc-20231231_g48.jpg (GRAPHIC) — 20KB

- fmcc-20231231_g49.jpg (GRAPHIC) — 19KB

- fmcc-20231231_g5.jpg (GRAPHIC) — 64KB

- fmcc-20231231_g50.jpg (GRAPHIC) — 37KB

- fmcc-20231231_g51.jpg (GRAPHIC) — 24KB

- fmcc-20231231_g52.jpg (GRAPHIC) — 18KB

- fmcc-20231231_g53.jpg (GRAPHIC) — 28KB

- fmcc-20231231_g54.jpg (GRAPHIC) — 23KB

- fmcc-20231231_g55.jpg (GRAPHIC) — 19KB

- fmcc-20231231_g56.jpg (GRAPHIC) — 18KB

- fmcc-20231231_g57.jpg (GRAPHIC) — 25KB

- fmcc-20231231_g58.jpg (GRAPHIC) — 22KB

- fmcc-20231231_g59.jpg (GRAPHIC) — 19KB

- fmcc-20231231_g6.jpg (GRAPHIC) — 36KB

- fmcc-20231231_g60.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g61.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g62.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g63.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g64.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g65.jpg (GRAPHIC) — 4KB

- fmcc-20231231_g66.jpg (GRAPHIC) — 4KB

- fmcc-20231231_g67.jpg (GRAPHIC) — 4KB

- fmcc-20231231_g68.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g69.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g7.jpg (GRAPHIC) — 34KB

- fmcc-20231231_g70.jpg (GRAPHIC) — 7KB

- fmcc-20231231_g71.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g72.jpg (GRAPHIC) — 5KB

- fmcc-20231231_g8.jpg (GRAPHIC) — 41KB

- fmcc-20231231_g9.jpg (GRAPHIC) — 33KB

- letterheada.jpg (GRAPHIC) — 33KB

- logoa.jpg (GRAPHIC) — 3KB

- 0001026214-24-000025.txt ( ) — 45232KB

- fmcc-20231231.xsd (EX-101.SCH) — 134KB

- fmcc-20231231_cal.xml (EX-101.CAL) — 105KB

- fmcc-20231231_def.xml (EX-101.DEF) — 853KB

- fmcc-20231231_lab.xml (EX-101.LAB) — 1459KB

- fmcc-20231231_pre.xml (EX-101.PRE) — 1091KB

- fmcc-20231231_htm.xml (XML) — 6368KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS 13

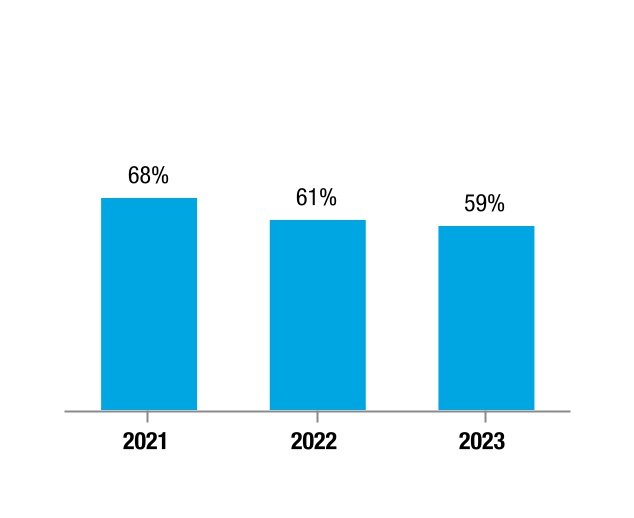

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS 13 n Housing and Mortgage Market Conditions 13 n Consolidated Results of Operations 15 n Consolidated Balance Sheets Analysis 21 n Our Portfolios 22 n Our Business Segments 24 n Risk Management 49 l Credit Risk 52 l Market Risk 79 l Operational Risk 84 n Liquidity and Capital Resources 89 n Conservatorship and Related Matters 101 n Regulation and Supervision 104 n Critical Accounting Estimates 111 RISK FACTORS 112 LEGAL PROCEEDINGS 131 MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES 132

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA 133

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA 133 n Report of Independent Registered Public Accounting Firm (PCAOB ID 238 ) 134 n Consolidated Financial Statements 136

CONTROLS AND PROCEDURES 217

CONTROLS AND PROCEDURES 217 OTHER INFORMATION 219 DIRECTORS, CORPORATE GOVERNANCE, AND EXECUTIVE OFFICERS 220 n Directors 220 n Corporate Governance 228 n Executive Officers 239

EXECUTIVE COMPENSATION 242

EXECUTIVE COMPENSATION 242 n Compensation Discussion and Analysis 242 n Compensation and Risk 257 n CEO Pay Ratio 258 n 2023 Compensation Information for NEOs 259

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS 265

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS 265 CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS 267 PRINCIPAL ACCOUNTING FEES AND SERVICES 269 EXHIBITS AND FINANCIAL STATEMENT SCHEDULES 271 GLOSSARY 272 EXHIBIT INDEX 280 SIGNATURES 286 FORM 10-K INDEX 288 FREDDIE MAC | 2023 Form 10-K i Table of Contents MD&A Table Index MD&A TABLE INDEX Table Description Page 1 Summary of Consolidated Statements of Income and Comprehensive Income 15 2 Components of Net Interest Income 15 3 Analysis of Net Interest Yield 17 4 Net Interest Income Rate / Volume Analysis 18 5 Components of Non-Interest Income 19 6 (Provision) Benefit for Credit Losses 19 7 Components of Non-Interest Expense 20 8 Summarized Consolidated Balance Sheets 21 9 Mortgage Portfolio 22 10 Mortgage-Related Investments Portfolio 23 11 Other Investments Portfolio 23 12 Single-Family Segment Financial Results 39 13 Multifamily Segment Financial Results 48 14 Allowance for Credit Losses Activity 53 15 Allowance for Credit Losses Ratios 53 16 Principal Amounts Due for Held-for-Investment Loans 54 17 Single-Family New Business Activity 57 18 Single-Family Mortgage Portfolio Newly Acquired Credit Enhancements 58 19 Single-Family Mortgage Portfolio Credit Enhancement Coverage Outstanding 59 20 Serious Delinquency Rates for Credit-Enhanced and Non-Credit-Enhanced Loans in Our Single-Family Mortgage Portfolio 59 21 Credit Enhancement Coverage by Year of Origination 60 22 Single-Family Mortgage Portfolio Without Credit Enhancement 60 23 Credit Quality Characteristics of Our Single-Family Mortgage Portfolio 62 24 Characteristics of the Loans in Our Single-Family Mortgage Portfolio 63 25 Single-Family Mortgage Portfolio Attribute Combinations 64 26 Seriously Delinquent Single-Family Loans 65 27 Single-Family Relief Refinance Loans 66 28 Single-Family Completed Loan Workout Activity 66 29 Credit Cha