Hartford Financial Services Group, Inc. Files 2023 Annual Report

Ticker: HIG-PG · Form: 10-K · Filed: Feb 23, 2024 · CIK: 874766

| Field | Detail |

|---|---|

| Company | Hartford Financial Services Group, INC. (HIG-PG) |

| Form Type | 10-K |

| Filed Date | Feb 23, 2024 |

| Risk Level | medium |

| Pages | 14 |

| Reading Time | 17 min |

| Key Dollar Amounts | $0.01, $72.02, $76.8 billion, $15.3 b, $24,527 b |

| Sentiment | neutral |

Sentiment: neutral

Topics: 10-K, Annual Report, Insurance, Financials, Hartford

TL;DR

<b>The Hartford Financial Services Group, Inc. has submitted its comprehensive 2023 annual report detailing financial performance and business operations.</b>

AI Summary

HARTFORD FINANCIAL SERVICES GROUP, INC. (HIG-PG) filed a Annual Report (10-K) with the SEC on February 23, 2024. The Hartford Financial Services Group, Inc. filed its 10-K annual report for the fiscal year ending December 31, 2023. The filing covers the period from January 1, 2023, to December 31, 2023. Key financial data and business operations for 2023 are detailed in the report. The company's principal business is Fire, Marine & Casualty Insurance. The report was filed on February 23, 2024.

Why It Matters

For investors and stakeholders tracking HARTFORD FINANCIAL SERVICES GROUP, INC., this filing contains several important signals. This 10-K filing provides investors with a detailed overview of The Hartford's financial health, operational strategies, and risk factors for the fiscal year 2023, enabling informed investment decisions. The report's disclosures are crucial for understanding the company's position within the Fire, Marine & Casualty Insurance sector and its outlook for future performance.

Risk Assessment

Risk Level: medium — HARTFORD FINANCIAL SERVICES GROUP, INC. shows moderate risk based on this filing. The filing is a standard 10-K annual report, which inherently contains a broad range of financial and operational information, but lacks specific forward-looking guidance or immediate material events that would elevate the risk level beyond medium.

Analyst Insight

Review the detailed financial statements and risk factors within the 10-K to assess The Hartford's performance and potential challenges in the insurance sector.

Key Numbers

- 20231231 — Fiscal Year End (Conformed Period of Report)

- 20240223 — Filing Date (Filed as of Date)

- 6331 — SIC Code (Standard Industrial Classification)

- 001-13958 — SEC File Number (SEC File Number)

Key Players & Entities

- HARTFORD FINANCIAL SERVICES GROUP, INC. (company) — Filer

- 0000874766 (company) — Central Index Key

- 6331 (company) — Standard Industrial Classification

- DE (company) — State of Incorporation

- CT (company) — State of Business Address

- 8605475000 (company) — Business Phone

- 20231231 (date) — Conformed Period of Report

- 20240223 (date) — Filed as of Date

FAQ

When did HARTFORD FINANCIAL SERVICES GROUP, INC. file this 10-K?

HARTFORD FINANCIAL SERVICES GROUP, INC. filed this Annual Report (10-K) with the SEC on February 23, 2024.

What is a 10-K filing?

A 10-K is a comprehensive annual financial report required by the SEC, covering audited financials, business operations, risk factors, and management discussion. This particular 10-K was filed by HARTFORD FINANCIAL SERVICES GROUP, INC. (HIG-PG).

Where can I read the original 10-K filing from HARTFORD FINANCIAL SERVICES GROUP, INC.?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by HARTFORD FINANCIAL SERVICES GROUP, INC..

What are the key takeaways from HARTFORD FINANCIAL SERVICES GROUP, INC.'s 10-K?

HARTFORD FINANCIAL SERVICES GROUP, INC. filed this 10-K on February 23, 2024. Key takeaways: The Hartford Financial Services Group, Inc. filed its 10-K annual report for the fiscal year ending December 31, 2023.. The filing covers the period from January 1, 2023, to December 31, 2023.. Key financial data and business operations for 2023 are detailed in the report..

Is HARTFORD FINANCIAL SERVICES GROUP, INC. a risky investment based on this filing?

Based on this 10-K, HARTFORD FINANCIAL SERVICES GROUP, INC. presents a moderate-risk profile. The filing is a standard 10-K annual report, which inherently contains a broad range of financial and operational information, but lacks specific forward-looking guidance or immediate material events that would elevate the risk level beyond medium.

What should investors do after reading HARTFORD FINANCIAL SERVICES GROUP, INC.'s 10-K?

Review the detailed financial statements and risk factors within the 10-K to assess The Hartford's performance and potential challenges in the insurance sector. The overall sentiment from this filing is neutral.

How does HARTFORD FINANCIAL SERVICES GROUP, INC. compare to its industry peers?

The Hartford operates within the Fire, Marine & Casualty Insurance industry, a sector characterized by its sensitivity to economic conditions, regulatory oversight, and claims management.

Are there regulatory concerns for HARTFORD FINANCIAL SERVICES GROUP, INC.?

As a financial services company, The Hartford is subject to extensive regulation by state insurance departments and federal agencies, impacting its operations, capital requirements, and product offerings.

Industry Context

The Hartford operates within the Fire, Marine & Casualty Insurance industry, a sector characterized by its sensitivity to economic conditions, regulatory oversight, and claims management.

Regulatory Implications

As a financial services company, The Hartford is subject to extensive regulation by state insurance departments and federal agencies, impacting its operations, capital requirements, and product offerings.

What Investors Should Do

- Analyze the company's financial statements for revenue trends, profitability, and balance sheet strength.

- Review the risk factors section to understand potential threats to the company's business and financial condition.

- Examine management's discussion and analysis (MD&A) for insights into operational performance and strategic priorities.

Key Dates

- 2023-12-31: Fiscal Year End — Marks the end of the reporting period for the 10-K.

- 2024-02-23: Filing Date — Date the 10-K was officially filed with the SEC.

Year-Over-Year Comparison

This filing is the annual 10-K report for fiscal year 2023, providing a comprehensive update compared to previous filings.

Filing Stats: 4,232 words · 17 min read · ~14 pages · Grade level 20 · Accepted 2024-02-23 16:32:34

Key Financial Figures

- $0.01 — ich registered Common Stock, par value $0.01 per share HIG The New York Stock Exchan

- $72.02 — billion, based on the closing price of $72.02 per share of the Common Stock on the Ne

- $76.8 billion — ockholders' equity of The Hartford were $76.8 billion and $15.3 billion, respectively. ORGA

- $15.3 b — of The Hartford were $76.8 billion and $15.3 billion, respectively. ORGANIZATION Th

- $24,527 b — a Corporate category. 2023 Revenues of $24,527 by Segment [1]Includes Revenue of $62 f

- $62 — 527 by Segment [1]Includes Revenue of $62 for Property & Casualty Other Operation

- $114 — roperty & Casualty Other Operations and $114 for Corporate. The following discussio

- $11,641 b — MERCIAL LINES 2023 Earned Premiums of $11,641 by Line of Business 2023 Earned Premium

- $20 — businesses with an annual payroll under $20, revenues under $50 and property values

- $50 — nnual payroll under $20, revenues under $50 and property values less than $20 per l

Filing Documents

- hig-20231231.htm (10-K) — 10156KB

- hig12312023-10xkex414.htm (EX-4.14) — 104KB

- hig12312023-10xkex1009.htm (EX-10.09) — 139KB

- hig12312023-10xkex1014.htm (EX-10.14) — 40KB

- hig12312023-10xkex1016.htm (EX-10.16) — 154KB

- hig12312023-10xkex1021.htm (EX-10.21) — 110KB

- hig12312023-10xkex1022.htm (EX-10.22) — 122KB

- hig12312023-10xkex2101.htm (EX-21.01) — 15KB

- hig12312023-10xkex2301.htm (EX-23.01) — 8KB

- hig12312023-10xkex2401.htm (EX-24.01) — 11KB

- hig12312023-10xkex3101.htm (EX-31.01) — 12KB

- hig12312023-10xkex3102.htm (EX-31.02) — 12KB

- hig12312023-10xkex3201.htm (EX-32.01) — 6KB

- hig12312023-10xkex3202.htm (EX-32.02) — 6KB

- hig12312023-10xkex9701.htm (EX-97.01) — 43KB

- hig-20231231_g1.jpg (GRAPHIC) — 49KB

- hig-20231231_g10.jpg (GRAPHIC) — 39KB

- hig-20231231_g11.jpg (GRAPHIC) — 46KB

- hig-20231231_g12.jpg (GRAPHIC) — 37KB

- hig-20231231_g13.jpg (GRAPHIC) — 48KB

- hig-20231231_g14.jpg (GRAPHIC) — 66KB

- hig-20231231_g15.jpg (GRAPHIC) — 104KB

- hig-20231231_g16.jpg (GRAPHIC) — 10KB

- hig-20231231_g17.jpg (GRAPHIC) — 9KB

- hig-20231231_g18.jpg (GRAPHIC) — 11KB

- hig-20231231_g19.jpg (GRAPHIC) — 9KB

- hig-20231231_g2.jpg (GRAPHIC) — 906KB

- hig-20231231_g20.jpg (GRAPHIC) — 9KB

- hig-20231231_g21.jpg (GRAPHIC) — 9KB

- hig-20231231_g22.jpg (GRAPHIC) — 54KB

- hig-20231231_g23.jpg (GRAPHIC) — 64KB

- hig-20231231_g24.jpg (GRAPHIC) — 42KB

- hig-20231231_g25.jpg (GRAPHIC) — 43KB

- hig-20231231_g26.jpg (GRAPHIC) — 43KB

- hig-20231231_g27.jpg (GRAPHIC) — 28KB

- hig-20231231_g28.jpg (GRAPHIC) — 24KB

- hig-20231231_g29.jpg (GRAPHIC) — 59KB

- hig-20231231_g3.jpg (GRAPHIC) — 48KB

- hig-20231231_g30.jpg (GRAPHIC) — 62KB

- hig-20231231_g31.jpg (GRAPHIC) — 20KB

- hig-20231231_g32.jpg (GRAPHIC) — 45KB

- hig-20231231_g33.jpg (GRAPHIC) — 20KB

- hig-20231231_g34.jpg (GRAPHIC) — 23KB

- hig-20231231_g35.jpg (GRAPHIC) — 33KB

- hig-20231231_g36.jpg (GRAPHIC) — 34KB

- hig-20231231_g37.jpg (GRAPHIC) — 26KB

- hig-20231231_g38.jpg (GRAPHIC) — 38KB

- hig-20231231_g39.jpg (GRAPHIC) — 27KB

- hig-20231231_g4.jpg (GRAPHIC) — 43KB

- hig-20231231_g40.jpg (GRAPHIC) — 24KB

- hig-20231231_g41.jpg (GRAPHIC) — 48KB

- hig-20231231_g42.jpg (GRAPHIC) — 29KB

- hig-20231231_g43.jpg (GRAPHIC) — 25KB

- hig-20231231_g44.jpg (GRAPHIC) — 26KB

- hig-20231231_g45.jpg (GRAPHIC) — 24KB

- hig-20231231_g46.jpg (GRAPHIC) — 23KB

- hig-20231231_g5.jpg (GRAPHIC) — 67KB

- hig-20231231_g6.jpg (GRAPHIC) — 48KB

- hig-20231231_g7.jpg (GRAPHIC) — 39KB

- hig-20231231_g8.jpg (GRAPHIC) — 37KB

- hig-20231231_g9.jpg (GRAPHIC) — 45KB

- image_0.jpg (GRAPHIC) — 6KB

- image_01.jpg (GRAPHIC) — 6KB

- 0000874766-24-000016.txt ( ) — 54585KB

- hig-20231231.xsd (EX-101.SCH) — 142KB

- hig-20231231_cal.xml (EX-101.CAL) — 179KB

- hig-20231231_def.xml (EX-101.DEF) — 1598KB

- hig-20231231_lab.xml (EX-101.LAB) — 2056KB

- hig-20231231_pre.xml (EX-101.PRE) — 1795KB

- hig-20231231_htm.xml (XML) — 11305KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

SIGNATURES

SIGNATURES 228 [a] The information required by this item is set forth in the Enterprise Risk Management section of Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations and is incorporated herein by reference. [b] See Index to Consolidated Financial Statements and Schedules elsewhere herein. [c] The information called for by Item 11 will be set forth in the Proxy Statement under the subcaptions "Compensation Discussion and Analysis", "Executive Compensation Tables", "Director Compensation", "Report of the Compensation and Management Development Committee", "Pay Versus Performance" and "CEO Pay Ratio" and is incorporated herein by reference. [d] Any information called for by Item 13 will be set forth in the Proxy Statement under the caption and subcaption "Board and Governance Matters" and "Director Independence" and is incorporated herein by reference. [e] The information called for by Item 14 will be set forth in the Proxy Statement under the caption "Audit Matters" and is incorporated herein by reference. 3

Forward-looking Statements

Forward-looking Statements Certain of the statements contained herein are forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as "anticipates," "intends," "plans," "seeks," "believes," "estimates," "expects," "projects," and similar references to future periods. Forward-looking statements are based on management's current expectations and assumptions regarding future economic, competitive, legislative and other developments and their potential effect upon The Hartford Financial Services Group, Inc. and its subsidiaries (collectively, the "Company" or "The Hartford"). Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. Actual results could differ materially from expectations depending on the evolution of various factors, including the risks and uncertainties identified below, as well as factors described in such forward-looking statements; or in Part I, Item 1A, Risk Factors, in Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations, and those identified from time to time in our other filings with the Securities and Exchange Commission . Risks Relating to Economic, Political and Global Market Conditions: challenges related to the Company's current operating environment, including global political, economic and market conditions, and the effect of financial market disruptions, economic downturns, changes in trade regulation including tariffs and other barriers or other potentially adverse macroeconomic developments on the demand for our products and returns in our investment portfolios; market risks associated with our business, including changes in credit spreads, equity prices, interest rates, inflation rate, foreign currency exchange rates and market volatility; the

- Item 1. Business

Part I - Item 1. Business Item 1.

BUSINESS

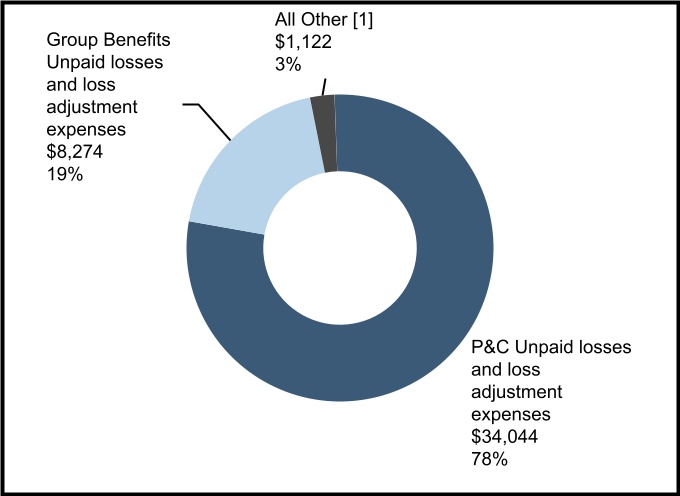

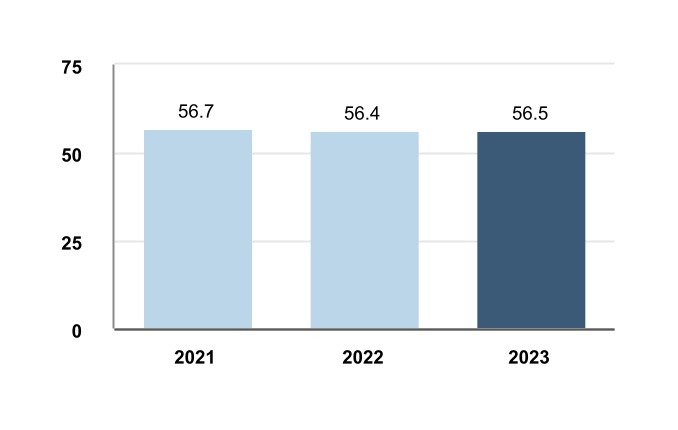

BUSINESS (Dollar amounts in millions, except for per share data, unless otherwise stated) Index Description Page General 6 Organization 6 Purpose and Strategic Priorities 6 Reporting Segments and Corporate 8 Reserves 17 Underwriting for P&C and Group Benefits 18 Claims Administration for P&C and Group Benefits 18 Reinsurance 18 Investment Operations 18 Enterprise Risk Management 19 Regulation and Intellectual Property 19 Human Capital Resources 20 Available Information 22 GENERAL The Hartford Financial Services Group, Inc. ("HFSG") (together with its subsidiaries, "The Hartford", the "Company", "we", or "our") is a holding company for a group of subsidiaries that provide property and casualty ("P&C") insurance, group benefits insurance and services, and mutual funds and exchange-traded funds ("ETF") to individual and business customers in the United States as well as in the United Kingdom and other international locations. The Hartford is headquartered in Connecticut and its oldest subsidiary, Hartford Fire Insurance Company, dates back to 1810. As of December 31, 2023, total assets and total stockholders' equity of The Hartford were $76.8 billion and $15.3 billion, respectively. ORGANIZATION The Hartford strives to maintain and enhance its position as a market leader within the financial services industry. The Company sells diverse and innovative products through multiple distribution channels to individuals and businesses and is considered a leading property and casualty and group benefits insurer. The Hartford Stag logo is one of the most recognized symbols in the financial services industry. As a holding company, The Hartford Financial Services Group, Inc. is separate and distinct from its subsidiaries and has no significant business operations of its own. The holding company relies on the dividends from its insurance companies and other subsidiaries as the principal source of cash flow to meet its obligations,

- Item 1. Business

Part I - Item 1. Business Strategic Priorities Our strategy remains consistent and we are focused on the following priorities across our businesses: Advancing leading underwriting capabilities across our portfolio to offer expanded products and services; Embracing a culture of growth and innovation and cross-enterprise collaboration; Emphasizing digital capabilities and data science that enhance the customer experience and improve underwriting and claims decision making; Maximizing distribution channels and product breadth to increase market share; Optimizing organizational efficiency with a focus on continuous improvement; Balancing use of excess capital for growth initiatives, investments in the business, and return to stockholders through dividends and share repurchases; and Continuing to advance sustainability leadership in order to attract and retain top talent and enhance value to stockholders. For more information on retaining and attracting talent through our diversity, equity and inclusion ("DEI") initiatives, refer to the Human Capital Resources section of Part 1, Item 1. Within our businesses, in 2024 we will continue to pursue objectives specific to each, including: Commercial Lines Maintaining underwriting and pricing discipline across property and liability lines of business; Continuing to broaden our underwriting capabilities, product breadth, and risk appetite, increasing the cross-sell of global specialty product lines to customers of small commercial and middle & large commercial, and growing specialized verticals in middle & large commercial; Accelerating use of data and digital technology, including artificial intelligence, and voice of customer to drive a best-in-class experience; Enabling improved risk selection and portfolio decisions through data science and analytics; and Expanding distribution to match customers' preferred access points. Personal Lines Regaining competitive momentum through the continued rollout of our n

- Item 1. Business

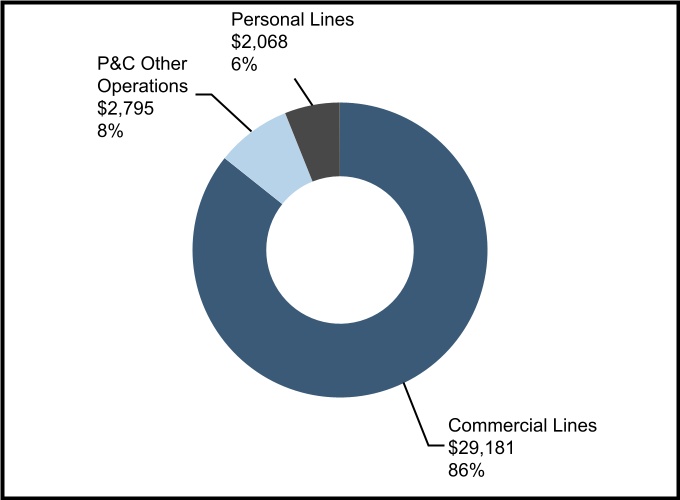

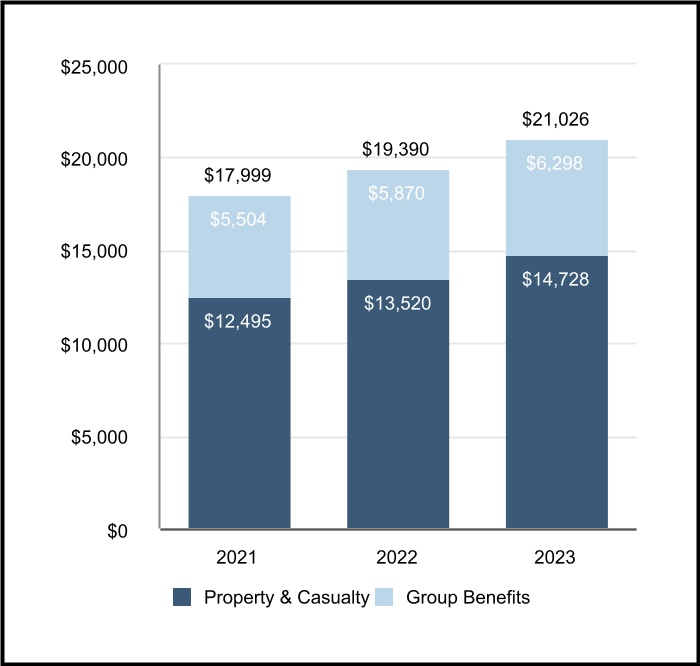

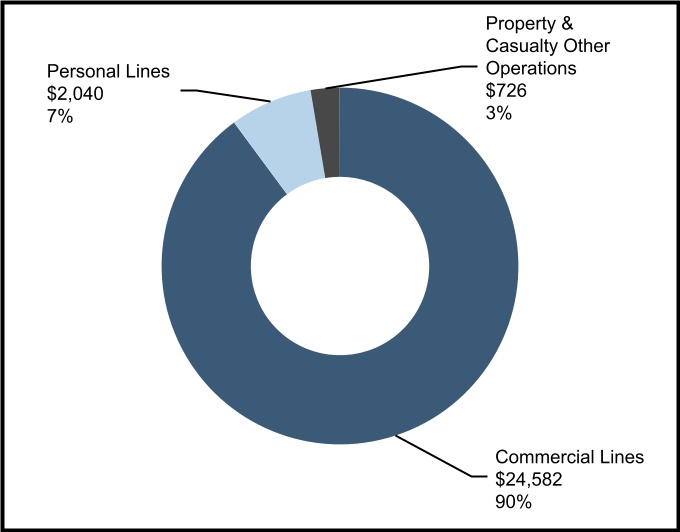

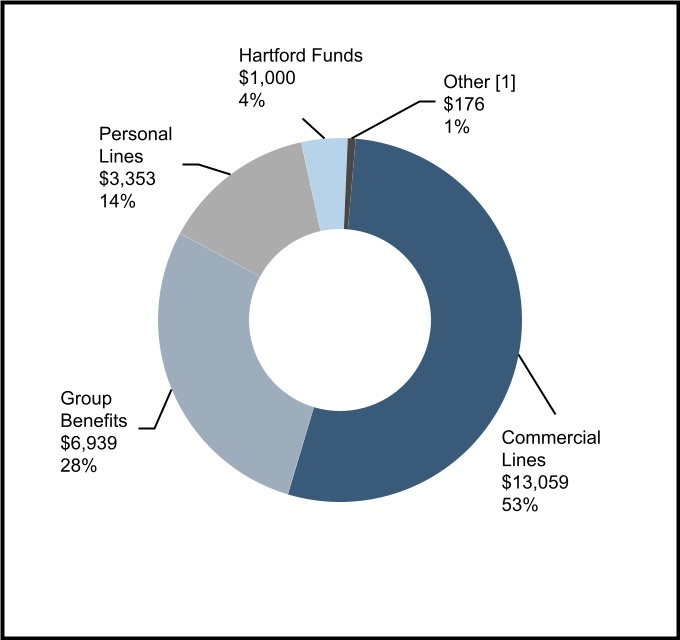

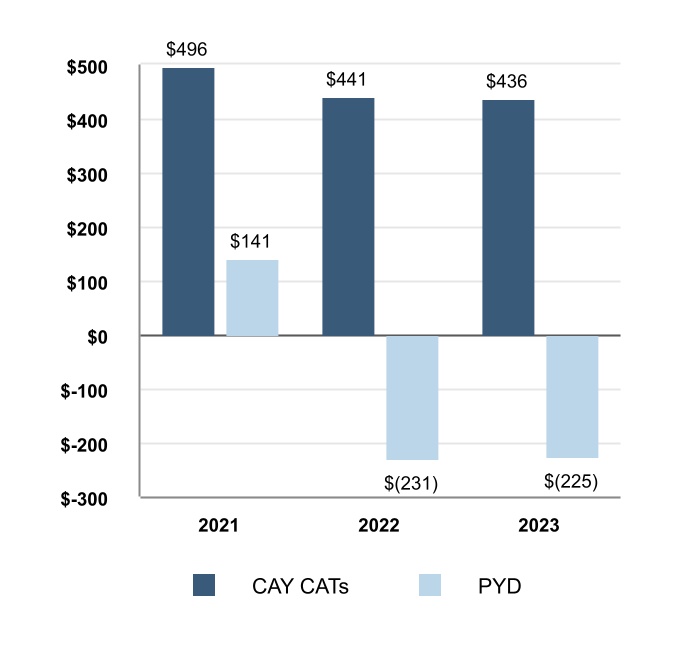

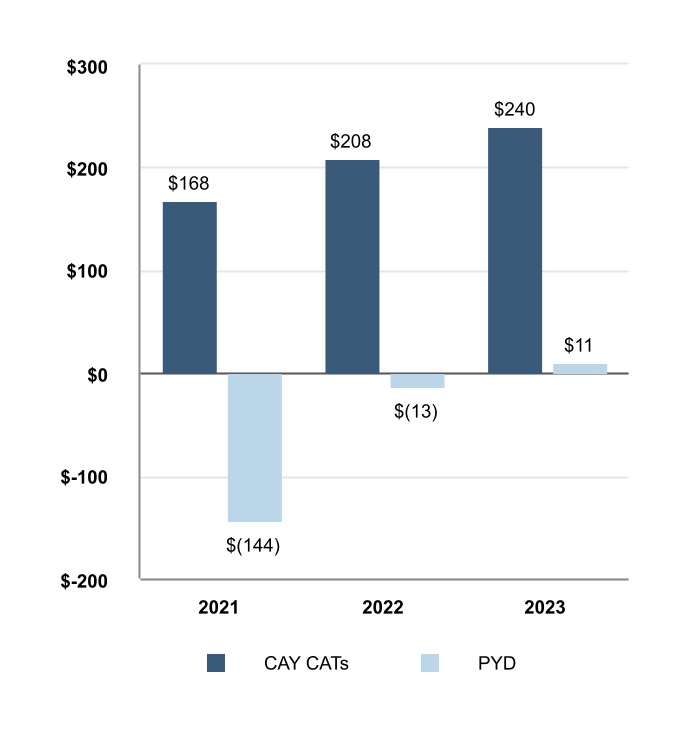

Part I - Item 1. Business Group Benefits Grow revenues in all customer segments with an emphasis on employer groups with under 500 lives; Expanding absence/leave management capabilities and pursuing product and service innovation to meet the rapidly evolving needs of employers and employees; Continuing to grow market share of voluntary product offerings, including supplemental health coverage, as well as new state paid family and medical leave; Investing in technology that enhances the overall customer experience, supported by easy and accurate operations processes; and Advancing data and technology capabilities, including artificial intelligence, to unlock process improvement and enable agility. Hartford Funds Driving organic growth by focusing on key distribution channels and optimizing our product and distribution teams; and Working with subadvisors to launch innovative products that meet the needs of financial advisors and their clients. REPORTING SEGMENTS The Hartford conducts business principally in five reporting segments including Commercial Lines, Personal Lines, Property & Casualty Other Operations, Group Benefits and Hartford Funds, as well as a Corporate category. 2023 Revenues of $24,527 by Segment [1]Includes Revenue of $62 for Property & Casualty Other Operations and $114 for Corporate. The following discussion describes the principal products and services, marketing and distribution, and competition of The Hartford's reporting segments. For further discussion of the reporting segments, including financial disclosures of revenues by product line, net income (loss), and assets for each reporting segment, see Note 3 - Segment Information of Notes to Consolidated Financial Statements. 8 | Table of Contents Index to Business

- Item 1. Business

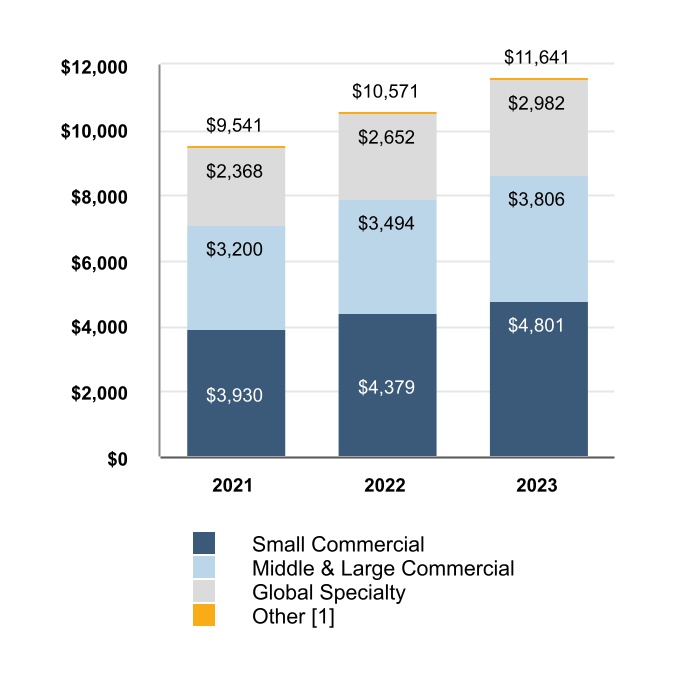

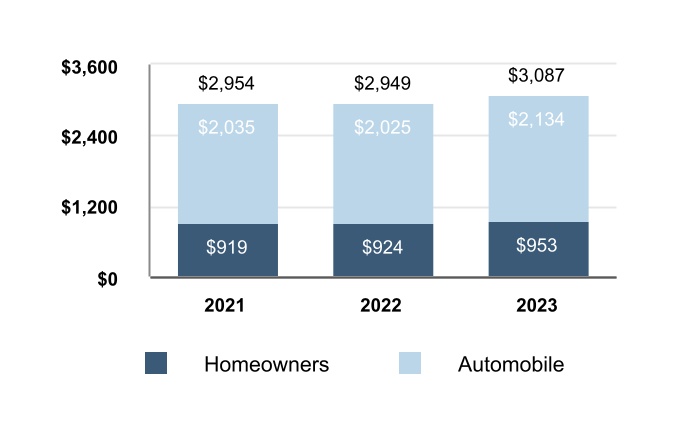

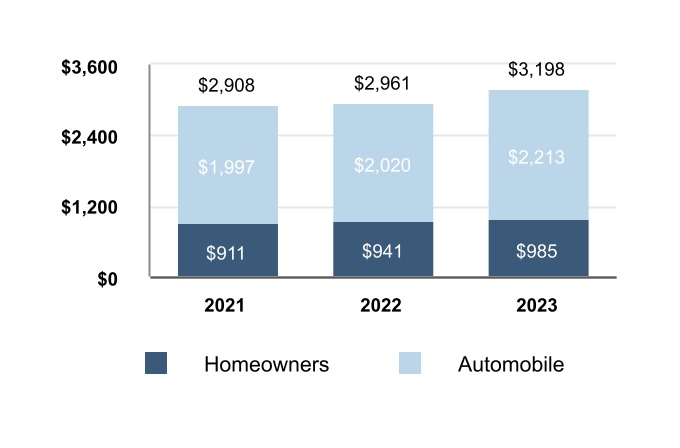

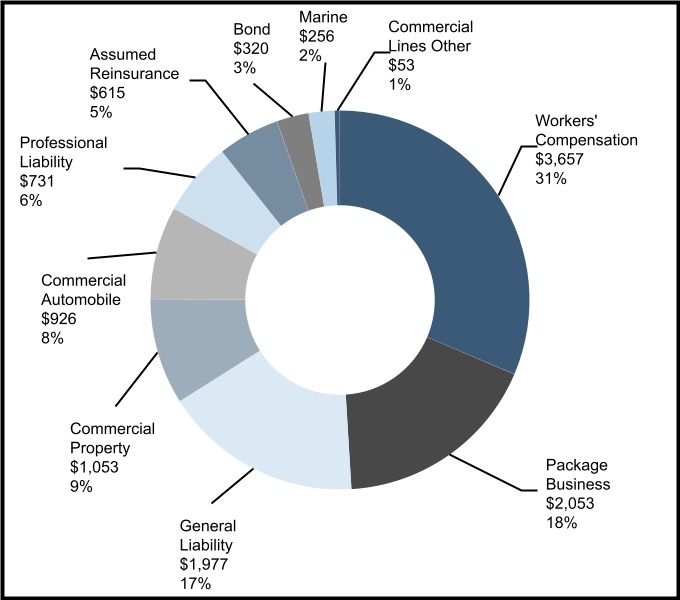

Part I - Item 1. Business | COMMERCIAL LINES 2023 Earned Premiums of $11,641 by Line of Business 2023 Earned Premiums of $11,641 by Product Principal Products and Services Automobile Covers damage to a business's fleet of vehicles due to collision or other perils (automobile physical damage). In addition to first party automobile physical damage, commercial automobile covers liability for bodily injuries and property damage suffered by third parties and losses caused by uninsured or under-insured motorists. Property Covers the building a business owns or leases as well as its personal property, including tools and equipment, inventory, and furniture. A commercial property insurance policy covers losses resulting from fire, wind, hail, earthquake, theft and other covered perils, including coverage for assets such as accounts receivable and valuable papers and records. Commercial property may include specialized equipment insurance, which provides coverage for loss or damage resulting from the mechanical breakdown of boilers and machinery. General Liability Covers a business in the event it is sued for causing harm to a person and/or damage to property. General liability insurance covers third-party claims arising from accidents occurring on the insured's premises or arising out of their operations. General liability insurance may also cover losses arising from product liability and provides replacement of lost income due to an event that interrupts business operations. Marine Encompasses various ocean and inland marine coverages including cargo, craft, hull, specie, transport and liability, among others. Package Business Covers both property and general liability damages. Workers' Compensation Covers employers for losses incurred due to employees sustaining an injury, illness or disability in connection with their work. Benefits paid under workers' compensation policies may include reimbursement of medical care costs, replacement income, compensation f

- Item 1. Business

Part I - Item 1. Business Through its three lines of business, small commercial, middle & large commercial, and global specialty, Commercial Lines offers its products and services to businesses in the United States ("U.S.") and internationally. Commercial Lines generally consists of products written for small businesses and middle market companies as well as national and multi-national accounts, largely distributed through retail agents and brokers, wholesale agents and global and specialty insurance and reinsurance brokers. The majority of Commercial Lines written premium is generated by small commercial and middle market lines, which provide coverage options and customized pricing based on the policyholder's individual risk characteristics. Small commercial and middle market lines within middle & large commercial are generally referred to as standard commercial lines. Small commercial provides coverages for small businesses, which the Company generally considers to be businesses with an annual payroll under $20, revenues under $50 and property values less than $20 per location. Primary coverages provided include workers' compensation, property, general liability and commercial automobile. Within small commercial, both property and general liability coverages are offered under a single package policy, marketed under the Spectrum name. Small commercial also provides excess and surplus lines coverage to small businesses including umbrella, general liability, property and other coverages. Middle & large commercial business provides insurance coverages to medium-sized and national accounts businesses, which are companies whose payroll, revenue and property values exceed the small business definition. In addition to offering standard commercial lines products, including workers' compensation, property, general liability and commercial automobile products, middle & large commercial includes program business which provides tailored programs, primarily to customers wit