UDR, Inc. Files Proxy Statement

Ticker: UDR · Form: DEFA14A · Filed: May 13, 2024 · CIK: 74208

| Field | Detail |

|---|---|

| Company | Udr, Inc. (UDR) |

| Form Type | DEFA14A |

| Filed Date | May 13, 2024 |

| Risk Level | low |

| Pages | 8 |

| Reading Time | 9 min |

| Key Dollar Amounts | $7 million, $38 |

| Sentiment | neutral |

Sentiment: neutral

Topics: proxy-statement, REIT, SEC-filing

TL;DR

UDR filed its proxy statement, shareholders vote soon.

AI Summary

UDR, Inc. filed a DEFA14A, which is a proxy statement, on May 13, 2024. This filing is an amendment to a previous filing and concerns matters related to the company's shareholder meeting. The company is a real estate investment trust (REIT) incorporated in Maryland.

Why It Matters

Proxy statements are crucial for shareholders as they contain important information about company proposals, executive compensation, and director nominations, enabling informed voting decisions.

Risk Assessment

Risk Level: low — This filing is a standard proxy statement (DEFA14A) and does not contain new material financial information or significant corporate actions that would inherently increase risk.

Key Numbers

- 1231 — Fiscal Year End (Indicates the end of UDR, Inc.'s fiscal year for reporting purposes.)

- 001-10524 — SEC File Number (UDR, Inc.'s SEC file number.)

Key Players & Entities

- UDR, Inc. (company) — Filer of the DEFA14A

- 0000074208-24-000046.txt (document) — Accession number for the filing

- 1934 Act (regulation) — Securities Exchange Act under which the filing is made

- MD (state) — State of incorporation for UDR, Inc.

FAQ

What is the purpose of a DEFA14A filing?

A DEFA14A filing is a Schedule 14A, a proxy statement, filed with the SEC by a company to solicit proxies from its shareholders for an upcoming meeting.

When was this DEFA14A filed by UDR, Inc.?

UDR, Inc. filed this DEFA14A on May 13, 2024.

What is UDR, Inc.'s Standard Industrial Classification (SIC) code?

UDR, Inc.'s SIC code is 6798, which corresponds to Real Estate Investment Trusts.

Where is UDR, Inc. headquartered?

UDR, Inc.'s business and mailing address is 1745 Shea Center Drive, Suite 200, Highlands Ranch, CO 80129.

What act governs this type of SEC filing?

This DEFA14A filing is made pursuant to Section 14(a) of the Securities Exchange Act of 1934.

Filing Stats: 2,296 words · 9 min read · ~8 pages · Grade level 16.3 · Accepted 2024-05-13 08:32:25

Key Financial Figures

- $7 million — . ISS incorrectly included a one-time $7 million equity grant to our CEO, granted in 202

- $38 — ing sales price of our common stock, or $38.29, on December 29, 2023, the last trad

Filing Documents

- tmb-20240513xdefa14a.htm (DEFA14A) — 70KB

- tmb-20240513xdefa14a001.jpg (GRAPHIC) — 1KB

- tmb-20240513xdefa14a004.jpg (GRAPHIC) — 31KB

- tmb-20240513xdefa14a005.jpg (GRAPHIC) — 26KB

- tmb-20240513xdefa14a006.jpg (GRAPHIC) — 31KB

- 0000074208-24-000046.txt ( ) — 194KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

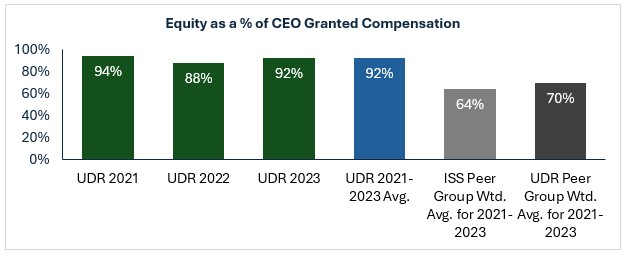

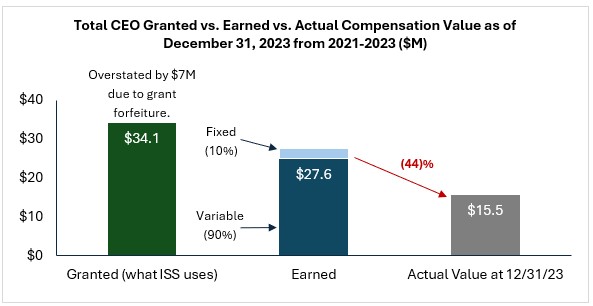

From the Filing

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 _______________________________________ SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) _________________________________ Filed by the Registrant Filed by a Party other than the Registrant Check the appropriate box: Preliminary Proxy Statement CONFIDENTIAL, FOR USE OF THE COMMISSION ONLY (AS PERMITTED BY RULE 14a-6(e)(2)) Definitive Proxy Statement Definitive Additional Materials Soliciting Material Pursuant to 240.14a-12 UDR, Inc. (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check all boxes that apply): No fee required. Fee paid previously with preliminary materials. Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. Beginning on or about May 13, 2024, UDR, Inc. ("UDR," the "Company," "we," or "our") made the following communication available to our shareholders. Advisory Vote on Executive Compensation. At the Company's 2024 annual meeting of shareholders to be held on Thursday, May 23, 2024, shareholders will cast an advisory vote on the compensation of the Company's named executive officers (the "Say on Pay Proposal"). There are two main proxy advisory firms, Institutional Shareholder Services Inc. ("ISS") and Glass, Lewis & Co. LLC ("Glass Lewis"), that issue their own respective reports and make recommendations for shareholder votes. We are pleased to have garnered favorable support and a recommendation by Glass Lewis to vote "FOR" on all proposals. Conversely, we are disappointed that ISS, for the first time since Say on Pay became effective in 2011, reached a different conclusion this year and has recommended that shareholders vote "AGAINST" our Say on Pay Proposal. As discussed in detail below, the Company's Board of Directors (the "Board") strongly disagrees with ISS's recommendation. Accordingly, the Board recommends that you vote " FOR " the approval of Proposal No. 2 – Advisory Vote on Executive Compensation. Regarding ISS's "AGAINST" Recommendation on the Say on Pay Proposal: The structure of our executive compensation program, which is 92% performance-based for our CEO, has not materially changed compared to the year prior, and in fact, has been consistent in design (although metrics and weightings for metrics have changed) for the past eight years . ISS has recommended a vote " FOR " with respect to our Say on Pay Proposal in each of the last 13 years (since Say on Pay was first included on our ballot) prior to this year. Glass Lewis recommended a "FOR" vote on UDR's Say on Pay Proposal, indicating amongst other things, that the structure of the executive compensation program is fair, the disclosure of its components is fair, and there is "alignment of pay with performance in the year in review." Approximately 90% of UDR shareholders have, on average, voted "FOR" our Say on Pay since Say on Pay was included on our ballot 13 years ago. The Compensation and Management Development Committee of UDR's Board of Directors (the "Committee") feels strongly that the executive compensation program has in the past and is expected in the future to continue to effectively align pay with performance and incentivize the continued creation of long-term value for shareholders. ISS's "AGAINST" recommendation is primarily based on what it perceives as a misalignment of Pay for Performance. We strongly disagree with this assessment because: UDR's Long-Term Incentive Plan is primarily driven by relative performance metrics versus our apartment peer group or an index and includes no time-based awards, which demonstrates strong alignment with the interests of UDR's shareholders. In addition, most of our peer group have a lower amount of "at risk" compensation. UDR's CEO has elected to take 100% of his short-term compensation (when combined with long-term compensation, this constitutes more than 90% of his total compensation) in some form of equity over the past three years, directly aligning his interests with the interests of our shareholders. Total compensation, as disclosed in the Summary Compensation Table of our Proxy Statement filed April 4, 2024 ("Granted Compensation"), does not equal earned compensation, as disclosed in our Proxy Statement, at the time of measurement or the value of that earned compensation as of December 31, 2023. Valuations for these metrics differ as a result of meeting or not meeting established rigorous performance targets as well as UDR's share price performance over time. Our CEO's earned compensation from 2021-2023 was significantly below his granted compensation (what ISS uses in its versus peer compensation analysis), and the value of that earned compensation as of December 31, 2023, was well below both granted and earned compensation from 2021-2023,