M&T Bank Corp. Files 2023 Annual Report on Form 10-K

Ticker: MTB-PK · Form: 10-K · Filed: Feb 21, 2024 · CIK: 36270

Sentiment: neutral

Topics: 10-K, Annual Report, M&T Bank, Financials, Banking

TL;DR

<b>M&T Bank Corp. has filed its comprehensive 2023 annual report (10-K) detailing its financial performance and operational landscape.</b>

AI Summary

M&T BANK CORP (MTB-PK) filed a Annual Report (10-K) with the SEC on February 21, 2024. M&T Bank Corp. filed its 10-K report for the fiscal year ending December 31, 2023. The filing covers the company's financial performance and operations for the year. Key financial data and disclosures are included in the report. The report details various aspects of the company's business, including its segments and financial instruments. M&T Bank Corp. is incorporated in New York and operates under the SIC code 6022 for Commercial Banks.

Why It Matters

For investors and stakeholders tracking M&T BANK CORP, this filing contains several important signals. This 10-K filing provides investors and stakeholders with a detailed overview of M&T Bank's financial health, strategic initiatives, and risk factors for the fiscal year 2023. Understanding the specifics within this report is crucial for assessing the bank's performance, its market position, and its outlook in the current economic environment.

Risk Assessment

Risk Level: medium — M&T BANK CORP shows moderate risk based on this filing. The filing is a standard annual report (10-K), which inherently contains a broad range of financial and operational information, but does not highlight any immediate, severe risks without further detailed analysis of its contents.

Analyst Insight

Review the detailed financial statements and risk factors within the 10-K to assess M&T Bank's performance and identify potential investment opportunities or concerns.

Key Numbers

- 20231231 — Fiscal Year End (Conformed Period of Report)

- 20240221 — Filing Date (Filed as of date)

- 189 — Public Document Count (Total documents in the filing)

Key Players & Entities

- M&T BANK CORP (company) — Filer name

- 0000036270 (company) — Central Index Key

- NY (company) — State of incorporation

- 6022 (company) — Standard Industrial Classification

- FIRST EMPIRE STATE CORP (company) — Former company name

- 19920703 (date) — Date of name change

FAQ

When did M&T BANK CORP file this 10-K?

M&T BANK CORP filed this Annual Report (10-K) with the SEC on February 21, 2024.

What is a 10-K filing?

A 10-K is a comprehensive annual financial report required by the SEC, covering audited financials, business operations, risk factors, and management discussion. This particular 10-K was filed by M&T BANK CORP (MTB-PK).

Where can I read the original 10-K filing from M&T BANK CORP?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by M&T BANK CORP.

What are the key takeaways from M&T BANK CORP's 10-K?

M&T BANK CORP filed this 10-K on February 21, 2024. Key takeaways: M&T Bank Corp. filed its 10-K report for the fiscal year ending December 31, 2023.. The filing covers the company's financial performance and operations for the year.. Key financial data and disclosures are included in the report..

Is M&T BANK CORP a risky investment based on this filing?

Based on this 10-K, M&T BANK CORP presents a moderate-risk profile. The filing is a standard annual report (10-K), which inherently contains a broad range of financial and operational information, but does not highlight any immediate, severe risks without further detailed analysis of its contents.

What should investors do after reading M&T BANK CORP's 10-K?

Review the detailed financial statements and risk factors within the 10-K to assess M&T Bank's performance and identify potential investment opportunities or concerns. The overall sentiment from this filing is neutral.

How does M&T BANK CORP compare to its industry peers?

M&T Bank Corp. operates within the commercial banking sector, a critical part of the financial services industry that provides a wide range of banking and financial services to individuals, businesses, and institutions.

Are there regulatory concerns for M&T BANK CORP?

As a commercial bank, M&T Bank Corp. is subject to extensive regulation by federal and state authorities, including the Federal Reserve and the New York State Department of Financial Services, governing its operations, capital adequacy, and consumer protection practices.

Industry Context

M&T Bank Corp. operates within the commercial banking sector, a critical part of the financial services industry that provides a wide range of banking and financial services to individuals, businesses, and institutions.

Regulatory Implications

As a commercial bank, M&T Bank Corp. is subject to extensive regulation by federal and state authorities, including the Federal Reserve and the New York State Department of Financial Services, governing its operations, capital adequacy, and consumer protection practices.

What Investors Should Do

- Analyze M&T Bank's revenue streams and growth drivers for FY2023.

- Evaluate the bank's asset quality and loan portfolio performance as detailed in the filing.

- Assess the bank's capital adequacy ratios and liquidity position.

Key Dates

- 2023-12-31: Fiscal Year End — Marks the end of the reporting period for the 10-K.

- 2024-02-21: Filing Date — Date M&T Bank Corp. submitted its 10-K filing.

Year-Over-Year Comparison

This is the initial filing for the fiscal year 2023, providing the latest comprehensive financial and operational data for M&T Bank Corp.

Filing Stats: 4,410 words · 18 min read · ~15 pages · Grade level 13.1 · Accepted 2024-02-21 16:37:54

Key Financial Figures

- $0.50 — nge on Which Registered Common Stock, $0.50 par value MTB New York Stock Exchan

- $250,000 — insured deposits and time deposits over $250,000 68 - 69 , 93 , 96 Item 1A. Risk F

- $100 billion — , and FDIC assigning each U.S. BHC with $100 billion or more in total consolidated assets to

- $208.3 b — ompany had consolidated total assets of $208.3 billion, deposits of $163.3 billion and s

- $163.3 billion — l assets of $208.3 billion, deposits of $163.3 billion and shareholders' equity of $27.0 billi

- $27.0 billion — 3.3 billion and shareholders' equity of $27.0 billion. The Company had 21,736 full-time and 4

- $207.8 b — T Bank had consolidated total assets of $207.8 billion, deposits of $167.3 billion and s

- $167.3 billion — l assets of $207.8 billion, deposits of $167.3 billion and shareholder's equity of $25.7 billi

- $25.7 billion — 7.3 billion and shareholder's equity of $25.7 billion. As a commercial bank, M&T Bank offers

- $683 m — mington Trust, N.A. had total assets of $683 million, deposits of $6 million and share

- $6 million — tal assets of $683 million, deposits of $6 million and shareholder's equity of $582 millio

- $582 million — $6 million and shareholder's equity of $582 million. M&T Securities is a wholly owned sub

- $56 million — 023, M&T Securities had total assets of $56 million and shareholder's equity of $55 million

- $55 million — $56 million and shareholder's equity of $55 million. M&T Securities recorded $13 million of

- $13 million — of $55 million. M&T Securities recorded $13 million of revenue in 2023. The headquarters of

Filing Documents

- mtb-20231231.htm (10-K) — 14086KB

- mtb-ex3_2.htm (EX-3.2) — 247KB

- mtb-ex4_2.htm (EX-4.2) — 52KB

- mtb-ex10_17.htm (EX-10.17) — 171KB

- mtb-ex10_22.htm (EX-10.22) — 24KB

- mtb-ex10_23.htm (EX-10.23) — 148KB

- mtb-ex23_1.htm (EX-23.1) — 3KB

- mtb-ex31_1.htm (EX-31.1) — 16KB

- mtb-ex31_2.htm (EX-31.2) — 15KB

- mtb-ex32_1.htm (EX-32.1) — 9KB

- mtb-ex32_2.htm (EX-32.2) — 10KB

- mtb-ex97_1.htm (EX-97.1) — 61KB

- img264708016_0.jpg (GRAPHIC) — 93KB

- img264708016_1.jpg (GRAPHIC) — 4KB

- img264708016_2.jpg (GRAPHIC) — 17KB

- img264708016_3.jpg (GRAPHIC) — 4KB

- 0000950170-24-017990.txt ( ) — 55806KB

- mtb-20231231.xsd (EX-101.SCH) — 4320KB

- mtb-20231231_htm.xml (XML) — 15515KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Business

Business 3 Disclosure pursuant to subpart 1400 of Regulation S-K I. Distribution of assets, liabilities, and shareholders' equity; interest rates and interest differential A. Average balance sheets 60 B. Interest income/expense and resulting yield or rate on average interest-earning assets and interestbearing liabilities 60 C. Rate/volume variances 61 II. Investments in debt securities A. Maturity schedule and weighted-average yield 94 III. Loan portfolio A. Maturity schedule 95 IV. Allowance for credit loss A. Credit ratios 74 - 75 Factors driving material changes in credit ratios or related components 73 - 83 , 141 - 147 B. Allocation of the allowance for credit losses 83 , 141 V. Deposits A. Average balances and rates 60 B. Uninsured deposits and time deposits over $250,000 68 - 69 , 93 , 96 Item 1A.

Risk Factors

Risk Factors 24 Item 1B. Unresolved Staff Comments 44 Item 1C. Cybersecurity 44 Item 2.

Properties

Properties 46 Item 3.

Legal Proceedings

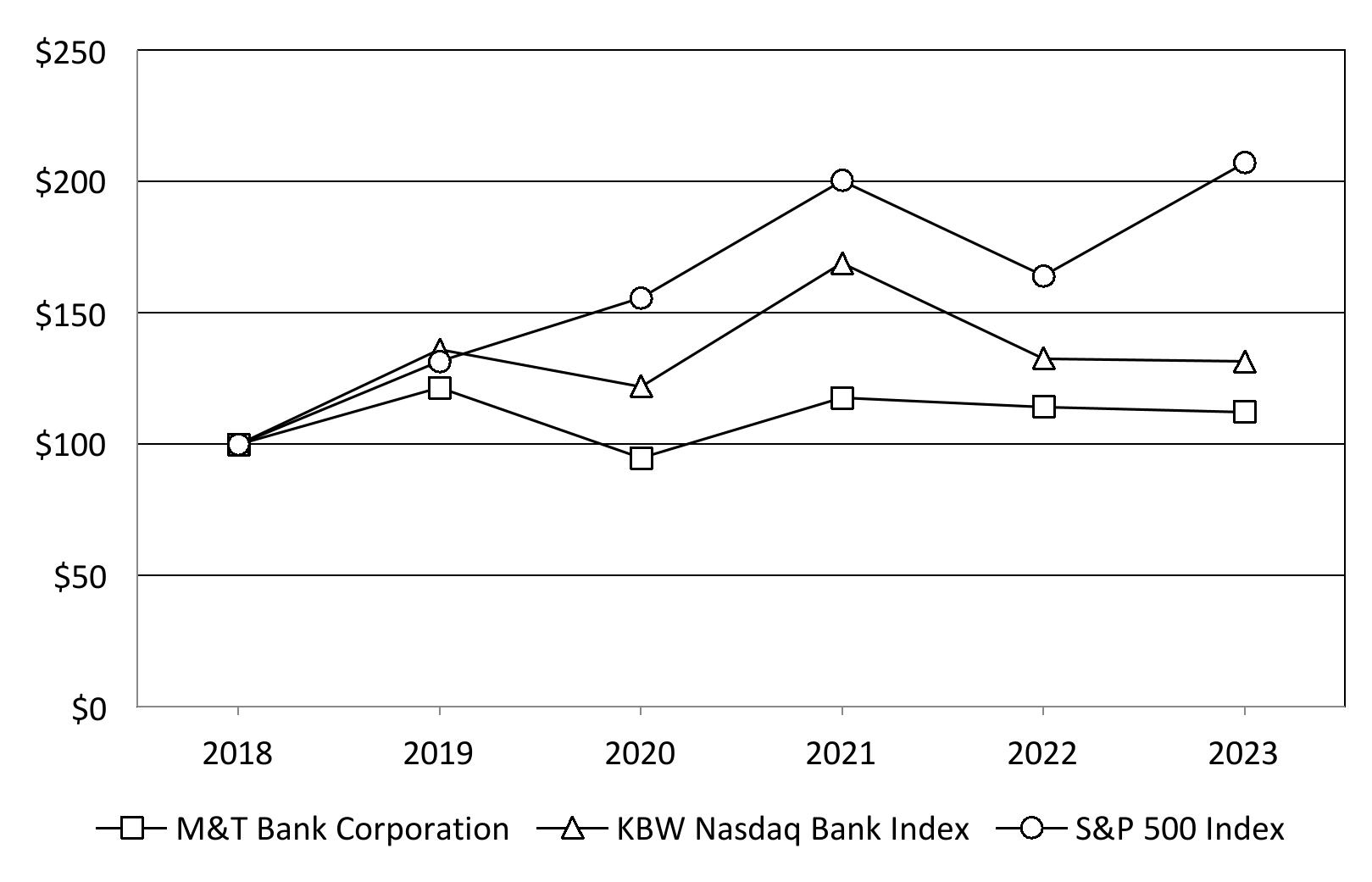

Legal Proceedings 47 Item 4. Mine Safety Disclosures 47 Executive Officers of the Registrant 47 PART II Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities 50 A. Principal market 50 B. Approximate number of holders at year-end 50 C. Frequency and amount of dividends declared 102 , 111 , 122 D. Restrictions on dividends 10 E. Securities authorized for issuance under equity compensation plans 50 F. Performance graph 51 G. Repurchases of common stock 52 Item 6.

Selected Financial Data

Selected Financial Data 52 Item 7.

Management's Discussion and Analysis of Financial Condition and Results of Operations

Management's Discussion and Analysis of Financial Condition and Results of Operations 52 Item 7A.

Quantitative and Qualitative Disclosures About Market Risk

Quantitative and Qualitative Disclosures About Market Risk 113 Item 8.

Financial Statements and Supplementary Data

Financial Statements and Supplementary Data 113 A. Report on Internal Control Over Financial Reporting 114 B. Report of Independent Registered Public Accounting Firm 115 C. Consolidated Balance Sheet — December 31, 2023 and 2022 118 D. Consolidated Statement of Income — Years ended December 31, 2023, 2022 and 2021 119 E. Consolidated Statement of Comprehensive Income — Years ended December 31, 2023, 2022 and 2021 120 F. Consolidated Statement of Cash Flows — Years ended December 31, 2023, 2022 and 2021 121 G. Consolidated Statement of Changes in Shareholders' Equity — Years ended December 31, 2023, 2022 and 2021 122 H.

Notes to Financial Statements

Notes to Financial Statements 123 I. Quarterly Trends 111 Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure 193 Item 9A.

Controls and Procedures

Controls and Procedures 193 A. Conclusions of principal executive officer and principal financial officer regarding disclosure controls and procedures 193 B. Management's annual report on internal control over financial reporting 193 C. Attestation report of the registered public accounting firm 193 D. Changes in internal control over financial reporting 193 Item 9B. Other Information 193 Item 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections 194 PART III Item 10. Directors, Executive Officers and Corporate Governance 194 Item 11.

Executive Compensation

Executive Compensation 194 Item 12.

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters 194 Item 13. Certain Relationships and Related Transactions, and Director Independence 195 Item 14. Principal Accountant Fees and Services 195 PART IV Item 15. Exhibits and Financial Statement Schedules 196 Item 16. Form 10-K Summary 198 S ignatures 199 Glossary of Terms The following listing includes acronyms and terms used throughout the document. Term Definition AML Anti-Money Laundering AMLA Anti-Money Laundering Act of 2020 Basel III Basel Committee's December 2010 final capital framework for strengthening international capital standards Bayview Financial Bayview Financial Holdings, L.P. together with its affiliates BHC Bank holding company BHCA Bank Holding Company Act of 1956, as amended BLG Bayview Lending Group, LLC BSA Bank Secrecy Act Capital Rules Capital adequacy standards established by the federal banking agencies CCyB Countercyclical capital buffer CET1 Common Equity Tier 1 CFPB Consumer Financial Protection Bureau CISO Chief Information Security Officer CIT Collective Investment Trust Common Securities Common securities issued in connection with the issuance of Junior Subordinated Debentures Company M&T Bank Corporation and its consolidated subsidiaries COVID-19 Coronavirus disease 2019 CRA Community Reinvestment Act of 1977 DIF Deposit Insurance Fund Dodd-Frank Act Dodd-Frank Wall Street Reform and Consumer Protection Act DUS Delegated Underwriting and Servicing EGRRCPA Economic Growth, Regulatory Relief, and Consumer Protection Act Exchange Act Securities Exchange Act of 1934 FASB Financial Accounting Standards Board FDIA Federal Deposit Insurance Act FDIC Federal Deposit Insurance Corporation Federal Reserve Board of Governors of the Federal Reserve System FHC Financial Holding Company FHLB Federal H

Business

Item 1. Business . M&T is a New York business corporation which is registered as a FHC under the BHCA and as a BHC under Article III-A of the New York Banking Law. The principal executive offices of M&T are located at One M&T Plaza, Buffalo, New York 14203. M&T was incorporated in November 1969. As of December 31, 2023, the Company had consolidated total assets of $208.3 billion, deposits of $163.3 billion and shareholders' equity of $27.0 billion. The Company had 21,736 full-time and 487 part-time employees as of December 31, 2023. At December 31, 2023, M&T had two wholly owned bank subsidiaries: M&T Bank and Wilmington Trust, N.A. The banks collectively offer a wide range of retail and commercial banking, trust and wealth management, and investment services to their customers. At December 31, 2023, M&T Bank represented over 99% of consolidated assets of the Company. On April 1, 2022, M&T completed the acquisition of People's United. Through its subsidiaries, People's United provided commercial banking, retail banking and wealth management services to individual, corporate and municipal customers through a network of branches located in Connecticut, southeastern New York, Massachusetts, Vermont, New Hampshire and Maine. Following the acquisition, People's United Bank, National Association, a national banking association and a wholly owned subsidiary of People's United, merged with and into M&T Bank, with M&T Bank as the surviving entity. The acquisition of People's United expanded the Company's geographical footprint and management expects the Company will benefit from greater geographical diversity and the advantages of scale associated with being a larger company. The Company from time to time considers acquiring banks, thrift institutions, branch offices of banks or thrift institutions, or other businesses within markets currently served by the Company or in other locations that would complement the Company's business or its geographic reach. The Company