Goosehead Insurance, Inc. Files 2023 Annual Report (10-K)

Ticker: GSHD · Form: 10-K · Filed: 2024-02-22T00:00:00.000Z

Sentiment: neutral

Topics: Goosehead Insurance, GSHD, 10-K, Annual Report, Financials

TL;DR

<b>Goosehead Insurance, Inc. has filed its 2023 10-K annual report detailing financial performance and corporate structure.</b>

AI Summary

Goosehead Insurance, Inc. (GSHD) filed a Annual Report (10-K) with the SEC on February 22, 2024. Goosehead Insurance, Inc. filed its 2023 10-K report on February 22, 2024. The filing covers the fiscal year ending December 31, 2023. Key financial data for 2023, 2022, and 2021 is included. The company's principal business address is in Westlake, TX. The filing includes details on common stock and additional paid-in capital.

Why It Matters

For investors and stakeholders tracking Goosehead Insurance, Inc., this filing contains several important signals. This 10-K filing provides a comprehensive overview of Goosehead's financial health and operational performance for the fiscal year 2023, crucial for investors assessing the company's trajectory. The detailed financial statements and disclosures within the report offer insights into revenue streams, capital structure, and potential risks, enabling stakeholders to make informed investment decisions.

Risk Assessment

Risk Level: — Goosehead Insurance, Inc. shows moderate risk based on this filing. The company operates in the insurance industry, which is subject to significant regulatory oversight and market fluctuations, as indicated by the nature of a 10-K filing.

Analyst Insight

Investors should review the detailed financial statements and risk factors in the 10-K to understand Goosehead Insurance's performance and outlook for 2024.

Revenue Breakdown

| Segment | Revenue | Growth |

|---|---|---|

| Commissions and Agency Fees | ||

| Franchise | ||

| Interest Income |

Key Numbers

- 2023-12-31 — Fiscal Year End (Reporting period)

- 2024-02-22 — Filing Date (Date of submission)

- 103 — Public Document Count (Number of documents in the filing)

Key Players & Entities

- Goosehead Insurance, Inc. (company) — Filer name

- 2024-02-22 (date) — Filing date

- 2023-12-31 (date) — Fiscal year end

- Westlake, TX (location) — Business address

- 10-K (document) — Form type

FAQ

When did Goosehead Insurance, Inc. file this 10-K?

Goosehead Insurance, Inc. filed this Annual Report (10-K) with the SEC on February 22, 2024.

What is a 10-K filing?

A 10-K is a comprehensive annual financial report required by the SEC, covering audited financials, business operations, risk factors, and management discussion. This particular 10-K was filed by Goosehead Insurance, Inc. (GSHD).

Where can I read the original 10-K filing from Goosehead Insurance, Inc.?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by Goosehead Insurance, Inc..

What are the key takeaways from Goosehead Insurance, Inc.'s 10-K?

Goosehead Insurance, Inc. filed this 10-K on February 22, 2024. Key takeaways: Goosehead Insurance, Inc. filed its 2023 10-K report on February 22, 2024.. The filing covers the fiscal year ending December 31, 2023.. Key financial data for 2023, 2022, and 2021 is included..

Is Goosehead Insurance, Inc. a risky investment based on this filing?

Based on this 10-K, Goosehead Insurance, Inc. presents a moderate-risk profile. The company operates in the insurance industry, which is subject to significant regulatory oversight and market fluctuations, as indicated by the nature of a 10-K filing.

What should investors do after reading Goosehead Insurance, Inc.'s 10-K?

Investors should review the detailed financial statements and risk factors in the 10-K to understand Goosehead Insurance's performance and outlook for 2024. The overall sentiment from this filing is neutral.

How does Goosehead Insurance, Inc. compare to its industry peers?

Goosehead Insurance operates in the insurance agents, brokers & services industry (SIC 6411). This sector involves facilitating insurance transactions and providing related services.

Are there regulatory concerns for Goosehead Insurance, Inc.?

As a publicly traded company, Goosehead Insurance is subject to the regulations of the Securities and Exchange Commission (SEC), requiring regular filings like the 10-K.

Industry Context

Goosehead Insurance operates in the insurance agents, brokers & services industry (SIC 6411). This sector involves facilitating insurance transactions and providing related services.

Regulatory Implications

As a publicly traded company, Goosehead Insurance is subject to the regulations of the Securities and Exchange Commission (SEC), requiring regular filings like the 10-K.

What Investors Should Do

- Analyze the detailed financial statements for revenue, net income, and other key performance indicators for fiscal year 2023.

- Review the risk factors section to understand potential challenges and their impact on the company's operations.

- Examine disclosures related to executive compensation and corporate governance.

Key Dates

- 2023-12-31: Fiscal Year End — End of the reporting period for the 10-K.

- 2024-02-22: Filing Date — Date Goosehead Insurance, Inc. submitted its 10-K filing.

Year-Over-Year Comparison

This is the initial analysis of the 2023 10-K filing; comparative data from previous filings will be assessed upon availability.

Filing Stats: 4,528 words · 18 min read · ~15 pages · Grade level 13.5 · Accepted 2024-02-21 20:37:13

Key Financial Figures

- $62.89 — ed using a closing price on that day of $62.89. As of February 19, 2024, there were

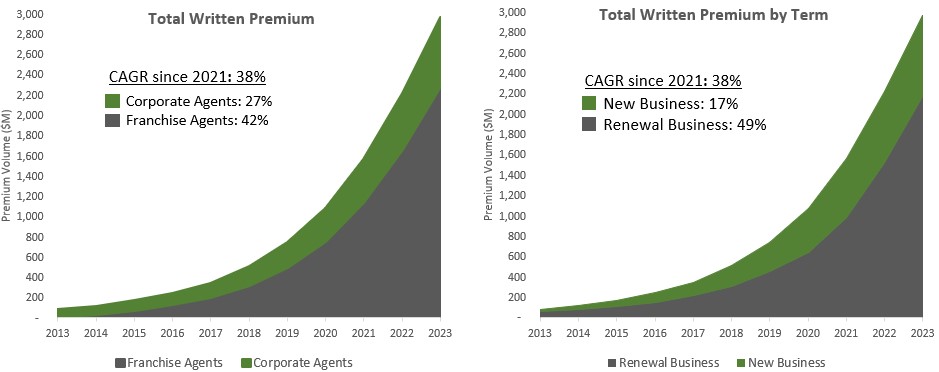

- $3.0 billion — of Contingent Commissions, grew 34% to $3.0 billion from $2.2 billion in 2022. This growth

- $2.2 billion — missions, grew 34% to $3.0 billion from $2.2 billion in 2022. This growth has been driven by

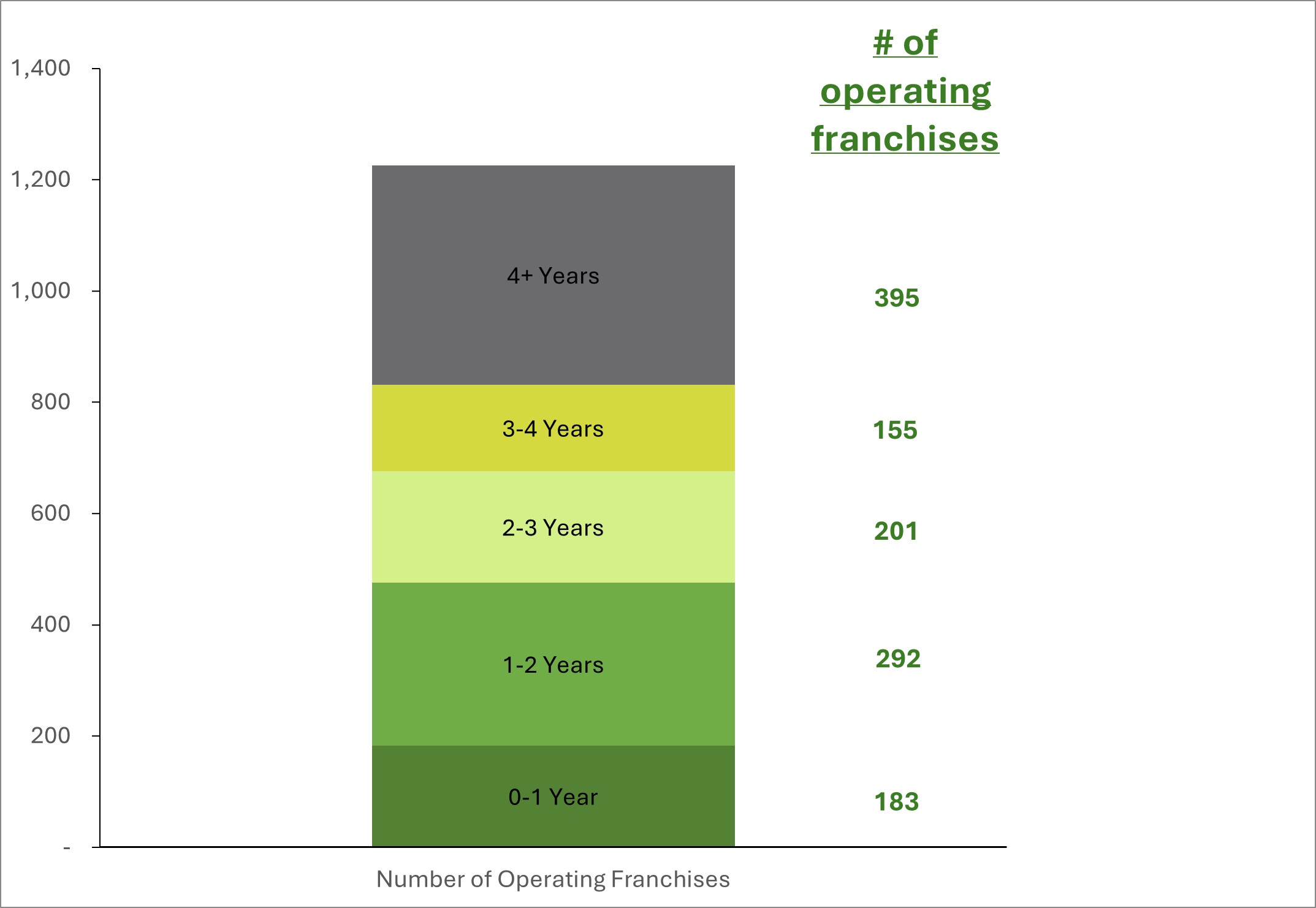

- $000 — w Business Revenue per agent by tenure ($000s) Source: Internal data for 2023; Car

- $73 thousand — uction per Agent in corporate sales was $73 thousand for agents with less than 1 year of ten

- $118 thousand — nts with less than 1 year of tenure and $118 thousand for agents with more than one year of t

- $38 thousand — New Business Production per Agency was $38 thousand for franchises with less than 1 year of

- $88 thousand — ses with less than 1 year of tenure and $88 thousand for franchises with more than one year

Filing Documents

- gshd-20231231.htm (10-K) — 1789KB

- a20231231-ex231consent.htm (EX-23.1) — 2KB

- a20231231-ex311.htm (EX-31.1) — 10KB

- a20231231-ex312.htm (EX-31.2) — 10KB

- a20231231-ex32.htm (EX-32) — 4KB

- ex97-nasdaqnonxfpiclawback.htm (EX-97) — 42KB

- gshd-20231231_g1.jpg (GRAPHIC) — 35KB

- gshd-20231231_g2.jpg (GRAPHIC) — 49KB

- gshd-20231231_g3.jpg (GRAPHIC) — 36KB

- gshd-20231231_g4.jpg (GRAPHIC) — 56KB

- gshd-20231231_g5.jpg (GRAPHIC) — 25KB

- gshd-20231231_g6.jpg (GRAPHIC) — 25KB

- gshd-20231231_g7.jpg (GRAPHIC) — 21KB

- gshd-20231231_g8.jpg (GRAPHIC) — 132KB

- gshd-20231231_g9.jpg (GRAPHIC) — 48KB

- 0001726978-24-000018.txt ( ) — 9477KB

- gshd-20231231.xsd (EX-101.SCH) — 63KB

- gshd-20231231_cal.xml (EX-101.CAL) — 92KB

- gshd-20231231_def.xml (EX-101.DEF) — 294KB

- gshd-20231231_lab.xml (EX-101.LAB) — 836KB

- gshd-20231231_pre.xml (EX-101.PRE) — 530KB

- gshd-20231231_htm.xml (XML) — 996KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Business

Item 1. Business 5

Risk factors

Item 1A. Risk factors 20

Unresolved staff comments

Item 1B. Unresolved staff comments 43

Cybersecurity

Item 1C. Cybersecurity 46

Properties

Item 2. Properties 45

Legal proceedings

Item 3. Legal proceedings 45

Mine safety disclosures

Item 4. Mine safety disclosures 45 PART II

Market for registrant's common equity, related stockholder matters and issuer purchases of equity securities

Item 5. Market for registrant's common equity, related stockholder matters and issuer purchases of equity securities 46

Reserved

Item 6. Reserved 48

Management's discussion and analysis of financial condition and results of operations

Item 7. Management's discussion and analysis of financial condition and results of operations 49

Quantitative and qualitative disclosure of market risks

Item 7A. Quantitative and qualitative disclosure of market risks 64

Financial statements and supplementary data

Item 8. Financial statements and supplementary data 65

Changes in and disagreements with accountants on accounting and financial statement disclosure

Item 9. Changes in and disagreements with accountants on accounting and financial statement disclosure 92

Controls and procedures

Item 9A. Controls and procedures 92

Other information

Item 9B. Other information 94

Disclosure regarding foreign jurisdictions that prevent inspections

Item 9C. Disclosure regarding foreign jurisdictions that prevent inspections 94 PART III

Directors, executive officers, and corporate governance

Item 10. Directors, executive officers, and corporate governance 95

Executive compensation

Item 11. Executive compensation 95

Security ownership of certain beneficial owners and management and related stockholder matters

Item 12. Security ownership of certain beneficial owners and management and related stockholder matters 95

Certain relationships and related transactions, and director independence

Item 13. Certain relationships and related transactions, and director independence 95

Principal accountant fees and services

Item 14. Principal accountant fees and services 95 PART IV

Exhibits and financial statement schedules

Item 15. Exhibits and financial statement schedules 96

Form 10-K summary

Item 16. Form 10-K summary 98

Signatures

Signatures 99 1 In this annual report on Form 10-K ("Annual Report"), "Goosehead," the "Company," "GSHD," "we," "us" and "our" refer to Goosehead Insurance, Inc. and its consolidated subsidiaries, including Goosehead Financial, LLC, together. Commonly used defined terms As used in this Annual Report, unless the context indicates or otherwise requires, the following terms have the following meanings: Ancillary Revenue: Revenue that is supplemental to our Core Revenue and Cost Recovery Revenue, Ancillary Revenue is unpredictable and often outside of the Company's control. Included in Ancillary Revenue are Contingent Commissions and other income. Agency Fees: Fees separate from commissions charged directly to clients for efforts performed in the issuance of new insurance policies. ASC 606 ("Topic 606"): ASU 2014-09 - Revenue from Contracts with Customers. Book of Business: Insurance policies bound by us with our Carriers on behalf of our clients. Best Practices Study: The industry group metrics are based on the latest date for which complete financial data are publicly available such as a 2023 Best Practices Study containing 2022 industry data conducted by Reagan Consulting and the Independent Insurance Agents & Brokers of America, Inc. Captive Agent: An insurance agent who only sells insurance policies for one Carrier. Carrier: An insurance company. Carrier Appointment: A contractual relationship with a Carrier. Client Retention: Calculated by comparing the number of all clients that had at least one policy in force twelve months prior to the date of measurement and still have at least one policy in force at the date of measurement. Contingent Commission: Revenue in the form of contractual payments from Carriers contingent upon several factors, including growth and profitability of the business placed with the Carrier. Core Revenue: The most predictable revenue stream for the Company, these revenues consist of New Business Revenue and Renewal Revenue

Business

Item 1. Business Company overview We are a rapidly growing independent insurance agency, reinventing the traditional approach to distributing personal lines policies throughout the United States. Our differentiated business model and innovative technology platform have enabled us to deliver insurance customers a superior experience, as evidenced by our 92 Net Promoter Score, which is 2.6x the 2022 P&C Industry Average according to Statista. To fully appreciate the value of our model, there are three lenses with which you can view us – from the perspective of 1) the insurance buyer; 2) the agent; and 3) the carrier. Insurance buyer perspective Insurance buyers desire to have the right coverage, based on their risk tolerance, at the lowest possible price, written with a reputable company who will respond quickly and fairly when they need to file a claim – desires that we believe only an independent insurance agent can fulfill. Clients want to accomplish this in a simple, fast, and convenient way that leverages technology to make the client experience effortless. We have built a model that combines a choice product portfolio, knowledgeable sales and service agents, and proprietary technology to deliver on these expectations. Choice product platform Today's insurance buyer expects choice; we believe that tomorrow's insurance buyer will demand it. We believe that most clients currently buying through single-product platforms are either over-paying or not properly covered because 1) their current insurance company does not offer the appropriate coverage or 2) valuable coverages were removed to make the pricing competitive. We are able to solve that by partnering with over 150 carriers and using technology to shop for our clients and quickly identify the Carrier who is targeting their segment of the market. This allows us to provide value by finding the right coverage at the lowest price, and to do so in one phone-call so that the client does not have to spend hours