Globe Life Inc. Files 2023 Annual Report on Form 10-K

Ticker: GL-PD · Form: 10-K · Filed: Feb 28, 2024 · CIK: 320335

Sentiment: neutral

Topics: Globe Life, 10-K, Annual Report, Life Insurance, Financials

TL;DR

<b>Globe Life Inc. has filed its comprehensive 2023 annual report (10-K), detailing its financial performance and operations in the life insurance sector.</b>

AI Summary

GLOBE LIFE INC. (GL-PD) filed a Annual Report (10-K) with the SEC on February 28, 2024. Globe Life Inc. filed its 2023 Form 10-K on February 28, 2024, reporting on the fiscal year ending December 31, 2023. The company's primary business is Life Insurance, with SIC code 6311. Globe Life Inc. is incorporated in Delaware and headquartered in McKinney, Texas. The filing covers the fiscal year from January 1, 2023, to December 31, 2023. Previous company names include Torchmark Corp and Liberty National Insurance Holding Co.

Why It Matters

For investors and stakeholders tracking GLOBE LIFE INC., this filing contains several important signals. This 10-K filing provides stakeholders with a detailed overview of Globe Life's financial health, operational performance, and strategic positioning for the fiscal year 2023. Understanding the specifics within this report is crucial for investors, analysts, and potential partners to assess the company's stability, growth prospects, and adherence to regulatory standards in the insurance industry.

Risk Assessment

Risk Level: medium — GLOBE LIFE INC. shows moderate risk based on this filing. The filing is a standard annual report (10-K) for a publicly traded company, which inherently carries market and operational risks common to the insurance industry, but does not highlight any immediate, severe financial distress or regulatory penalties.

Analyst Insight

Review the detailed financial statements and risk factors within the 10-K to assess Globe Life's performance and outlook for the upcoming fiscal year.

Revenue Breakdown

| Segment | Revenue | Growth |

|---|---|---|

| Life Insurance Segment | ||

| Health Insurance Product Line | ||

| Other Insurance Product Line |

Key Numbers

- 20231231 — Fiscal Year End (CONFORMED PERIOD OF REPORT)

- 20240228 — Filing Date (FILED AS OF DATE)

- 6311 — SIC Code (STANDARD INDUSTRIAL CLASSIFICATION)

- 3700 SOUTH STONEBRIDGE DRIVE — Business Address (STREET 1)

- 972-569-4000 — Business Phone (BUSINESS PHONE)

Key Players & Entities

- GLOBE LIFE INC. (company) — FILER

- TORCHMARK CORP (company) — FORMER COMPANY

- LIBERTY NATIONAL INSURANCE HOLDING CO (company) — FORMER COMPANY

- MCKINNEY (location) — BUSINESS ADDRESS CITY

- TX (location) — BUSINESS ADDRESS STATE

- DE (location) — STATE OF INCORPORATION

- 20231231 (date) — CONFORMED PERIOD OF REPORT

- 20240228 (date) — FILED AS OF DATE

FAQ

When did GLOBE LIFE INC. file this 10-K?

GLOBE LIFE INC. filed this Annual Report (10-K) with the SEC on February 28, 2024.

What is a 10-K filing?

A 10-K is a comprehensive annual financial report required by the SEC, covering audited financials, business operations, risk factors, and management discussion. This particular 10-K was filed by GLOBE LIFE INC. (GL-PD).

Where can I read the original 10-K filing from GLOBE LIFE INC.?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by GLOBE LIFE INC..

What are the key takeaways from GLOBE LIFE INC.'s 10-K?

GLOBE LIFE INC. filed this 10-K on February 28, 2024. Key takeaways: Globe Life Inc. filed its 2023 Form 10-K on February 28, 2024, reporting on the fiscal year ending December 31, 2023.. The company's primary business is Life Insurance, with SIC code 6311.. Globe Life Inc. is incorporated in Delaware and headquartered in McKinney, Texas..

Is GLOBE LIFE INC. a risky investment based on this filing?

Based on this 10-K, GLOBE LIFE INC. presents a moderate-risk profile. The filing is a standard annual report (10-K) for a publicly traded company, which inherently carries market and operational risks common to the insurance industry, but does not highlight any immediate, severe financial distress or regulatory penalties.

What should investors do after reading GLOBE LIFE INC.'s 10-K?

Review the detailed financial statements and risk factors within the 10-K to assess Globe Life's performance and outlook for the upcoming fiscal year. The overall sentiment from this filing is neutral.

Risk Factors

- Regulatory Compliance [medium — regulatory]: The company operates in a highly regulated industry, subject to state and federal laws and regulations impacting insurance operations.

- Market Conditions [medium — market]: Changes in economic conditions, interest rates, and competitive landscape can affect the company's financial performance and growth.

- Operational Risks [medium — operational]: Risks related to claims processing, policy administration, and technology infrastructure are inherent in the insurance business.

- Investment Risks [medium — financial]: The company's investment portfolio is subject to market fluctuations and credit risks, impacting profitability.

Filing Stats: 4,350 words · 17 min read · ~15 pages · Grade level 14.8 · Accepted 2024-02-28 17:17:26

Key Financial Figures

- $1.00 — ange on which registered Common Stock, $1.00 par value per share GL New York Stock E

- $4.3 million — ided financial support of approximately $4.3 million to organizations within that focus, inc

Filing Documents

- gl-20231231.htm (10-K) — 7316KB

- gli202310-kexhibit1028.htm (EX-10.28) — 38KB

- gli202310-kexhibit1053xq4.htm (EX-10.53) — 35KB

- gli202310-kexhibit1054xq4.htm (EX-10.54) — 54KB

- gli202310-kexhibit1055xq4.htm (EX-10.55) — 52KB

- gli202310-kexhibit1056xq4.htm (EX-10.56) — 30KB

- gli202310-kexhibit1057xq4.htm (EX-10.57) — 39KB

- gli202310-kexhibit1058xq4.htm (EX-10.58) — 70KB

- a10-kexhibit21q42023.htm (EX-21) — 7KB

- a10-kexhibit23q42023.htm (EX-23) — 2KB

- a10-kexhibit24q42023.htm (EX-24) — 60KB

- a10-kex311dardenq4fy2023.htm (EX-31.1) — 10KB

- a10-kex312svobodaq4fy2023.htm (EX-31.2) — 10KB

- a10-kex313kalmbachq4fy2023.htm (EX-31.3) — 10KB

- a10-kexhibit321allq4fy2023.htm (EX-32.1) — 8KB

- a10-kexhibit97q42023.htm (EX-97) — 26KB

- gl-20231231_g1.jpg (GRAPHIC) — 208KB

- gl-20231231_g10.jpg (GRAPHIC) — 46KB

- gl-20231231_g11.jpg (GRAPHIC) — 49KB

- gl-20231231_g12.jpg (GRAPHIC) — 37KB

- gl-20231231_g13.jpg (GRAPHIC) — 67KB

- gl-20231231_g2.jpg (GRAPHIC) — 167KB

- gl-20231231_g3.jpg (GRAPHIC) — 276KB

- gl-20231231_g4.jpg (GRAPHIC) — 275KB

- gl-20231231_g5.jpg (GRAPHIC) — 222KB

- gl-20231231_g6.jpg (GRAPHIC) — 104KB

- gl-20231231_g7.jpg (GRAPHIC) — 58KB

- gl-20231231_g8.jpg (GRAPHIC) — 62KB

- gl-20231231_g9.jpg (GRAPHIC) — 56KB

- gli202310-kexhibit1028001.jpg (GRAPHIC) — 271KB

- gli202310-kexhibit1028002.jpg (GRAPHIC) — 264KB

- gli202310-kexhibit1028003.jpg (GRAPHIC) — 261KB

- gli202310-kexhibit1028004.jpg (GRAPHIC) — 253KB

- gli202310-kexhibit1028005.jpg (GRAPHIC) — 250KB

- gli202310-kexhibit1028006.jpg (GRAPHIC) — 281KB

- gli202310-kexhibit1028007.jpg (GRAPHIC) — 269KB

- gli202310-kexhibit1028008.jpg (GRAPHIC) — 215KB

- 0000320335-24-000006.txt ( ) — 45556KB

- gl-20231231.xsd (EX-101.SCH) — 163KB

- gl-20231231_cal.xml (EX-101.CAL) — 208KB

- gl-20231231_def.xml (EX-101.DEF) — 974KB

- gl-20231231_lab.xml (EX-101.LAB) — 1757KB

- gl-20231231_pre.xml (EX-101.PRE) — 1371KB

- gl-20231231_htm.xml (XML) — 9664KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Risk Factors

Item 1A. Risk Factors 9

Unresolved Staff Comments

Item 1B. Unresolved Staff Comments 15

Cybersecurity

Item 1C. Cybersecurity 15

Properties

Item 2. Properties 16

Legal Proceedings

Item 3. Legal Proceedings 17

Mine Safety Disclosures

Item 4. Mine Safety Disclosures 17 PART II.

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

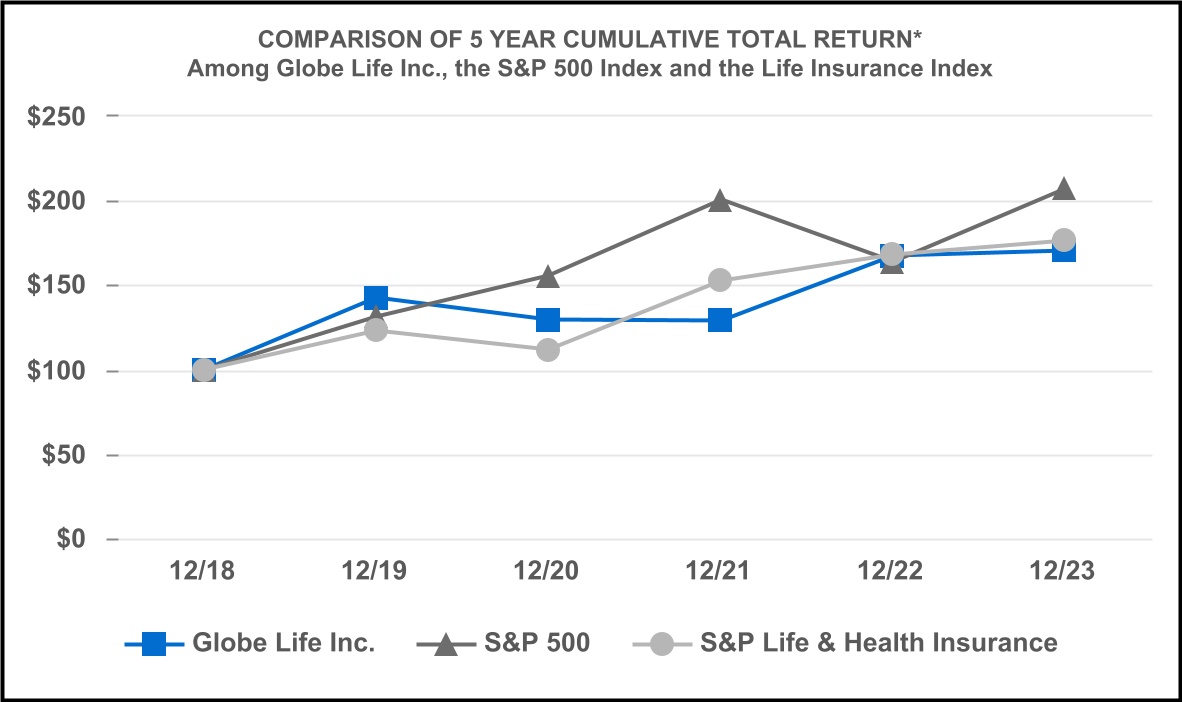

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities 18

[Reserved]

Item 6. [Reserved] 19 Cautionary Statements 20

Management's Discussion and Analysis of Financial Condition and Results of Operations

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations 21

Quantitative and Qualitative Disclosures about Market Risk

Item 7A. Quantitative and Qualitative Disclosures about Market Risk 53

Financial Statements and Supplementary Data

Item 8. Financial Statements and Supplementary Data 53 Consolidated Balance Sheets 57 Consolidated Statements of Operations 58 Consolidated Statements of Comprehensive Income 59 Consolidated Statements of Shareholders' Equity 60 Consolidated Statements of Cash Flows 61

Notes to Consolidated Financial Statements

Notes to Consolidated Financial Statements 62 Note 1—Significant Accounting Policies 62 Note 2—Statutory Accounting 77 Note 3—Supplemental Information about Changes to Accumulated Other Comprehensive Income 78 Note 4—Investments 80 Note 5—Commitments and Contingencies 93 Note 6—Policy Liabilities 96 Note 7—Deferred Acquisition Costs 111 Note 8—Liability for Unpaid Claims 114 Note 9—Income Taxes 115 Note 10—Postretirement Benefits 117 Note 11—Supplemental Disclosures of Cash Flow Information 124 Note 12—Debt 125 Note 13—Shareholders' Equity 127 Note 14—Stock-Based Compensation 128 Note 15—Business Segments 133 Note 16—Selected Quarterly Data (Unaudited) 140

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure 141

Controls and Procedures

Item 9A. Controls and Procedures 141

Other Information

Item 9B. Other Information 144

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections

Item 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections 144 PART III.

Directors, Executive Officers, and Corporate Governance

Item 10. Directors, Executive Officers, and Corporate Governance 144

Executive Compensation

Item 11. Executive Compensation 144

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters 144

Certain Relationships and Related Transactions and Director Independence

Item 13. Certain Relationships and Related Transactions and Director Independence 145

Principal Accountant Fees and Services

Item 14. Principal Accountant Fees and Services 145 PART IV.

Exhibits and Financial Statement Schedules

Item 15. Exhibits and Financial Statement Schedules 145

Signatures

Signatures 155 GL 2023 FORM 10-K Table of Contents Part I

Business

Item 1. Business Globe Life and the Company refer to Globe Life Inc., an insurance holding company incorporated in Delaware in 1979, and its subsidiaries and affiliates. Its primary subsidiaries are Globe Life And Accident Insurance Company, American Income Life Insurance Company, Liberty National Life Insurance Company, Family Heritage Life Insurance Company of America, and United American Insurance Company. Globe Life's website is: www.globelifeinsurance.com. Globe Life makes available free of charge through its website, its annual report on Form 10-K, its quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after they have been electronically filed with or furnished to the Securities and Exchange Commission. Other information included in Globe Life's website is not incorporated into this filing. 1 GL 2023 FORM 10-K Table of Contents The following table presents Globe Life's business by primary marketing distribution method. Additional information concerning industry segments may be found in Management's Discussion and Analysis and in Note 15—Business Segments within the Notes to the Consolidated Financial Statements . Primary Distribution Method Underwriting Company Products and Target Markets Distribution Direct to Consumer Division Globe Life And Accident Insurance Company McKinney, Texas Individual life and supplemental health limited-benefit insurance including juvenile and senior life coverage and Medicare Supplement to lower middle-income to middle-income Americans. Nationwide distribution through direct to consumer channels: including direct mail, electronic media, and insert media. American Income Life Division American Income Life Insurance Company Waco, Texas Individual life and supplemental health limited-benefit insurance marketed to working families. 10,579 average producing agents in the U.S., Canada, and New Zealand. Liberty National Division Liberty Na

Underwriting

Underwriting The underwriting standards of Globe Life's insurance subsidiaries are established by management. Each subsidiary uses information obtained from the application, and in some cases additional information such as, telephone interviews with applicants, inspection reports, pharmacy data, motor vehicle records, responses to both medical and non-medical questions, doctors' statements and/or medical examinations. This information is used to determine whether a policy should be issued in accordance with the application, with a different rating, with a rider, with reduced coverage, or rejected. Reserves The life insurance policy reserves reflected in Globe Life's consolidated financial statements as future policy benefits are calculated based on accounting principles generally accepted in the United States of America (GAAP). These reserves, with future premiums and the associated interest compounded at assumed rates, are expected to be sufficient to cover policy and contract obligations as they mature. Generally, the mortality and lapse assumptions used in the calculations of reserves are based on Company experience. Similar reserves are held on most of the health insurance policies written by Globe Life's insurance subsidiaries, since these policies generally are issued on a guaranteed-renewable basis. The assumptions used in the calculation of Globe Life's reserves are reported in Note 1—Significant Accounting Policies . Reserves for annuity products and certain life products consist of the policyholders' account values and are increased by policyholder deposits and interest credited and are decreased by policy charges and benefit payments. Reinsurance Globe Life has historically participated in very limited third-party reinsurance as a result of the low face amounts of the policies sold by the Company. See Schedule IV , Note 5—Commitments and Contingencies , Note 6—Policy Liabilities , and Note 8—Liability for Unpaid Claims for more information. In

Risk Factors

Item 1A. Risk Factors Risks Related to Our Business The following is a summary of the material risks and uncertainties that could adversely affect our business, financial condition and results of operations. Business and Operational Risks The development and maintenance of our various distribution channels are critical to growth in product sales and profits. Our future success depends, in substantial part, on our ability to recruit, hire, and motivate highly-skilled insurance personnel. Further, the development and retention of producing agents are critical to supporting sales growth in our agency operations because our insurance sales are primarily made to individuals. A failure to effectively develop new methods of reaching consumers, realize cost efficiencies or generate an attractive value proposition in our Direct to Consumer Division business could result in reduced sales and profits. In addition, if we do not provide an attractive career opportunity with competitive compensation as well as motivation for producing agents to increase sales of our products, our growth could be impeded. Doing so may be difficult due to many factors, including but not limited to, fluctuations in economic and industry conditions and the effectiveness of our compensation programs and competition among other companies. Our life insurance products are sold in niche markets. We are at risk should any of these markets diminish. We have several life distribution channels that focus on distinct market niches, three of which are labor unions, affinity groups, and sales via Direct to Consumer solicitations. Deterioration of our relationships with either organized labor union groups or affinity groups, or adverse changes in the public's receptivity to Direct to Consumer marketing initiatives could negatively affect our life insurance business. Actual or alleged misclassification of independent contractors at our insurance subsidiaries could result in adverse legal, tax or