FASTENAL CO Files Definitive Proxy Statement

Ticker: FAST · Form: DEF 14A · Filed: Mar 6, 2024

Sentiment: neutral

Topics: FASTENAL, Proxy Statement, DEF 14A, SEC Filing, Corporate Governance

TL;DR

<b>FASTENAL CO has filed its Definitive Proxy Statement for the period ending April 25, 2024.</b>

AI Summary

FASTENAL CO (FAST) filed a Proxy Statement (DEF 14A) with the SEC on March 6, 2024. FASTENAL CO filed a Definitive Proxy Statement on March 6, 2024. The filing covers the period ending April 25, 2024. The company's fiscal year ends on December 31. FASTENAL CO is incorporated in Minnesota. The company's business and mailing address is 2001 THEURER BLVD, WINONA, MN 55987.

Why It Matters

For investors and stakeholders tracking FASTENAL CO, this filing contains several important signals. This filing is a standard procedural document required for public companies to solicit proxies from shareholders for annual meetings. It provides detailed information on executive compensation, board of directors, and matters to be voted on by shareholders, which is crucial for investor understanding and participation.

Risk Assessment

Risk Level: low — FASTENAL CO shows low risk based on this filing. The filing is a routine proxy statement, indicating no immediate material changes or significant risks are being disclosed beyond standard corporate governance information.

Analyst Insight

Review the proxy statement for details on executive compensation, board nominations, and any shareholder proposals to understand management's strategy and potential changes.

Key Numbers

- 2024-03-06 — Filing Date (DEF 14A filing date)

- 2024-04-25 — Reporting Period End Date (Conformed period of report)

- 1231 — Fiscal Year End (Fiscal year end)

Key Players & Entities

- FASTENAL CO (company) — FILER

- 2024-04-25 (date) — CONFORMED PERIOD OF REPORT

- 2024-03-06 (date) — FILED AS OF DATE

- MN (location) — STATE OF INCORPORATION

- 1231 (date) — FISCAL YEAR END

- 2001 THEURER BLVD (address) — BUSINESS ADDRESS STREET 1

- WINONA (location) — BUSINESS ADDRESS CITY

- 55987 (postal_code) — BUSINESS ADDRESS ZIP

FAQ

When did FASTENAL CO file this DEF 14A?

FASTENAL CO filed this Proxy Statement (DEF 14A) with the SEC on March 6, 2024.

What is a DEF 14A filing?

A DEF 14A is a definitive proxy statement sent to shareholders before annual meetings, covering executive compensation, board nominations, and shareholder votes. This particular DEF 14A was filed by FASTENAL CO (FAST).

Where can I read the original DEF 14A filing from FASTENAL CO?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by FASTENAL CO.

What are the key takeaways from FASTENAL CO's DEF 14A?

FASTENAL CO filed this DEF 14A on March 6, 2024. Key takeaways: FASTENAL CO filed a Definitive Proxy Statement on March 6, 2024.. The filing covers the period ending April 25, 2024.. The company's fiscal year ends on December 31..

Is FASTENAL CO a risky investment based on this filing?

Based on this DEF 14A, FASTENAL CO presents a relatively low-risk profile. The filing is a routine proxy statement, indicating no immediate material changes or significant risks are being disclosed beyond standard corporate governance information.

What should investors do after reading FASTENAL CO's DEF 14A?

Review the proxy statement for details on executive compensation, board nominations, and any shareholder proposals to understand management's strategy and potential changes. The overall sentiment from this filing is neutral.

How does FASTENAL CO compare to its industry peers?

FASTENAL CO operates in the retail sector, specifically focusing on building materials, hardware, and garden supply.

Are there regulatory concerns for FASTENAL CO?

The filing is a DEF 14A, a Definitive Proxy Statement filed under the Securities Exchange Act of 1934, which requires public companies to provide shareholders with information for voting at meetings.

Industry Context

FASTENAL CO operates in the retail sector, specifically focusing on building materials, hardware, and garden supply.

Regulatory Implications

The filing is a DEF 14A, a Definitive Proxy Statement filed under the Securities Exchange Act of 1934, which requires public companies to provide shareholders with information for voting at meetings.

What Investors Should Do

- Review the proposals to be voted on by shareholders.

- Examine the details of executive compensation packages.

- Assess the nominees for the Board of Directors.

Year-Over-Year Comparison

This is a DEF 14A filing, which is a standard proxy statement and does not inherently represent a change from previous filings unless specific proposals or changes in governance are detailed within.

Filing Stats: 4,754 words · 19 min read · ~16 pages · Grade level 12.2 · Accepted 2024-03-06 10:50:32

Key Financial Figures

- $8.9 billion — marketer of recreational vehicles with $8.9 billion in annual revenues, since August 2015.

Filing Documents

- fast-20240306.htm (DEF 14A) — 1019KB

- fast-20240306_g1.jpg (GRAPHIC) — 115KB

- fast-20240306_g2.jpg (GRAPHIC) — 6KB

- fast-20240306_g3.jpg (GRAPHIC) — 17KB

- fast-20240306_g4.jpg (GRAPHIC) — 320KB

- fast-20240306_g5.jpg (GRAPHIC) — 390KB

- fast-20240306_g6.jpg (GRAPHIC) — 3KB

- fast-20240306_g7.jpg (GRAPHIC) — 143KB

- fast-20240306_g8.jpg (GRAPHIC) — 118KB

- 0000815556-24-000015.txt ( ) — 4253KB

- fast-20240306.xsd (EX-101.SCH) — 5KB

- fast-20240306_def.xml (EX-101.DEF) — 8KB

- fast-20240306_lab.xml (EX-101.LAB) — 12KB

- fast-20240306_pre.xml (EX-101.PRE) — 7KB

- fast-20240306_htm.xml (XML) — 97KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

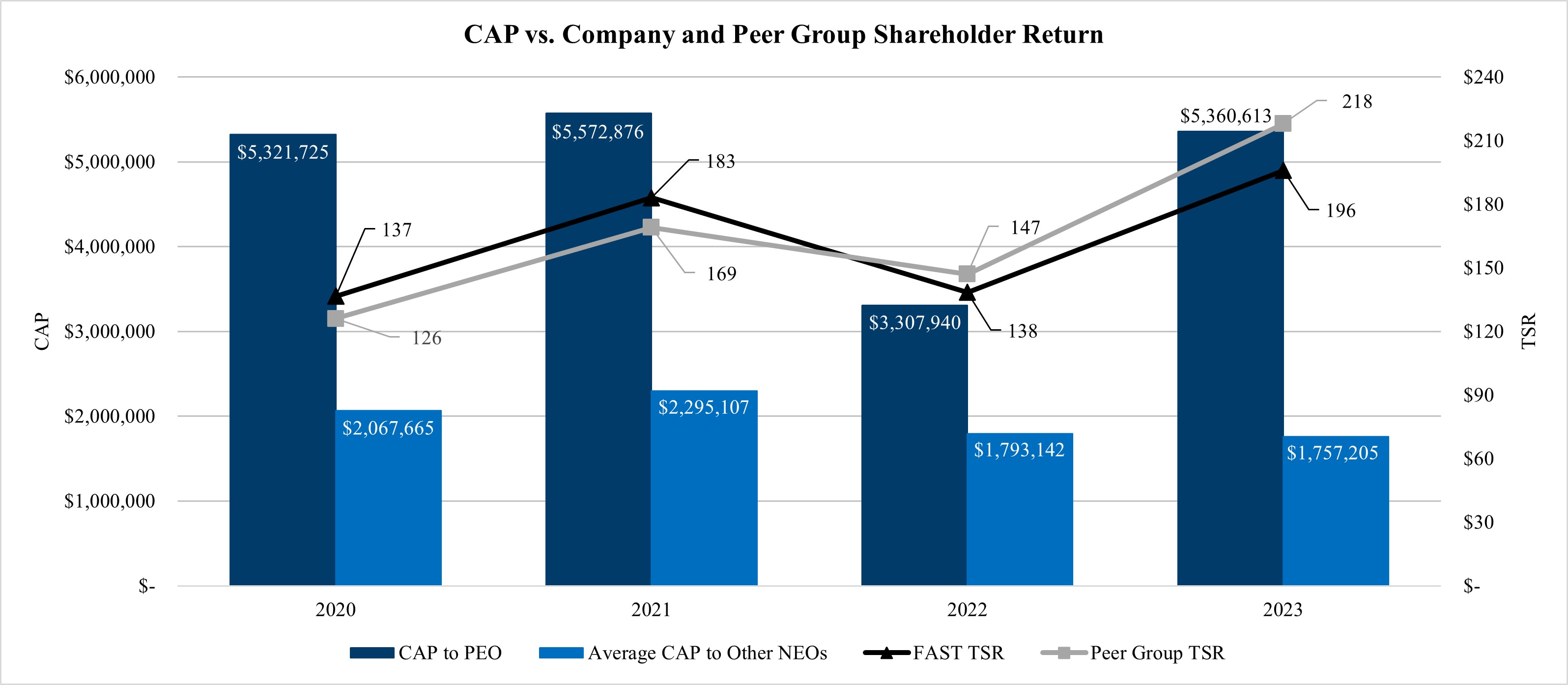

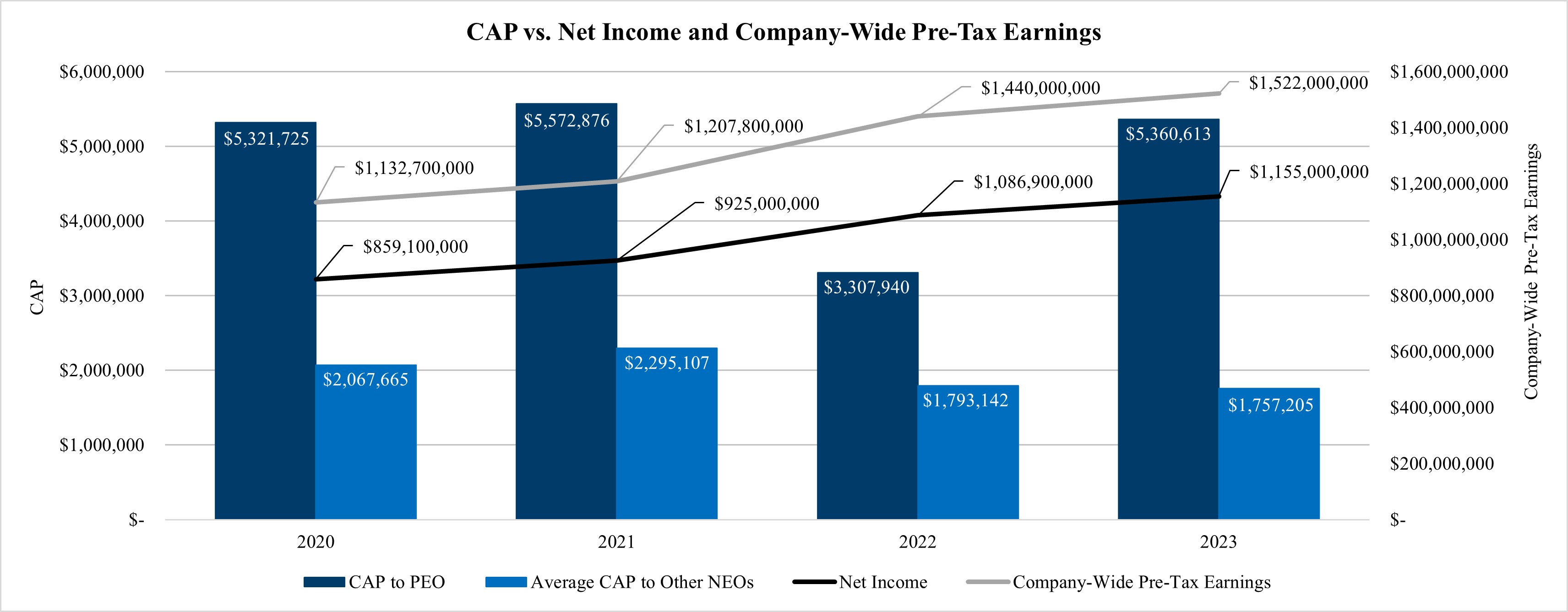

Executive compensation

Executive compensation 22 Proposal #4 – Approval of an amendment to our Restated Articles of Incorporation to delete Article VI regarding supermajority approval of business combinations with certain interested parties 43 Proposal # 5 – Shareholder proposal relating to simple majority vote 45

Security ownership of principal shareholders and management

Security ownership of principal shareholders and management 46 Additional matters 48 Householding 48 Deadlines for receipt of shareholder proposals and nominations for the 2025 annual meetin g 49

FORWARD-LOOKING STATEMENTS

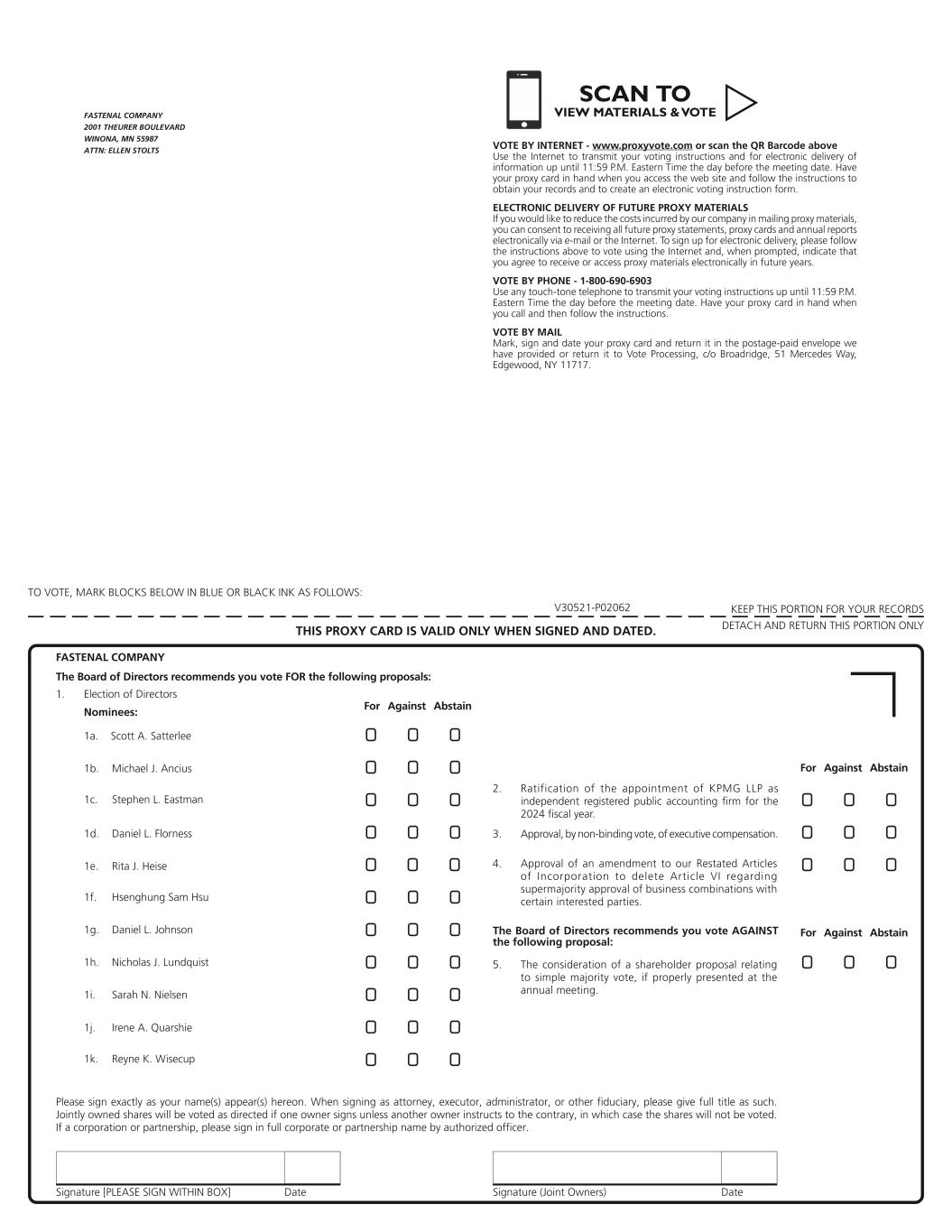

FORWARD-LOOKING STATEMENTS This proxy statement contains forward-looking information within the meaning of the Private Securities Litigation Reform Act of 1995 that is subject to certain risks and uncertainties that could cause actual results to differ materially from those projected, expressed, or implied by such forward-looking information. Risks and uncertainties that could cause or contribute to such differences include, but are not limited to, those discussed in Item 1A, "Risk Factors" included in our Annual Report on Form 10-K, as may be updated in our subsequent Quarterly Reports on Form 10-Q. To the extent permitted under applicable law, we assume no obligation to update any forward-looking statements as a result of new information or future events -1- Table of Cont ents GENERAL INFORMATION ABOUT THE MEETING AND VOTING What am I voting on? These are the proposals scheduled to be voted on at the annual meeting: Election of all eleven directors ('Proposal #1'); Ratification of the appointment of KPMG LLP as our independent registered public accounting firm for 2024 ('Proposal #2'); Adoption of a resolution approving, on an advisory, non-binding basis, the compensation of certain of our executive officers ('Proposal #3'); Approval of an amendment to our Restated Articles of Incorporation to delete Article VI regarding supermajority approval of business combinations with certain interested parties ('Proposal #4'); and Consideration of a shareholder proposal relating to simple majority vote ('Proposal #5'). Who is entitled to vote? The common stock of Fastenal, par value $.01 per share, is our only authorized and issued voting security. At the close of business on February 26, 2024, there were 572,426,650 shares of common stock issued and outstanding, each of which is entitled to one vote. Only shareholders of record at the close of business on February 26, 2024 will be entitled to vote at the annual meeting or any adjournments thereof. What cons