Avient Corp Files Definitive Proxy Statement

Ticker: AVNT · Form: DEF 14A · Filed: Mar 27, 2024

Sentiment: neutral

Topics: Proxy Statement, DEF 14A, Avient Corp, Corporate Governance, Executive Compensation

TL;DR

<b>Avient Corp has filed its Definitive Proxy Statement for the period ending May 16, 2024.</b>

AI Summary

AVIENT CORP (AVNT) filed a Proxy Statement (DEF 14A) with the SEC on March 27, 2024. Avient Corp filed a Definitive Proxy Statement (DEF 14A) on March 27, 2024. The filing covers the period ending May 16, 2024. The company's fiscal year ends on December 31. Avient Corp's former name was Polyone Corp, with a name change date of August 30, 2000. The filing includes information related to executive compensation for 2023.

Why It Matters

For investors and stakeholders tracking AVIENT CORP, this filing contains several important signals. This filing is crucial for shareholders to understand executive compensation, board nominations, and other corporate governance matters before the annual meeting. Shareholders will vote on key proposals, including the election of directors and executive compensation, which can impact the company's strategic direction and financial performance.

Risk Assessment

Risk Level: low — AVIENT CORP shows low risk based on this filing. The filing is a routine DEF 14A, indicating standard corporate governance and shareholder communication processes rather than immediate financial distress or significant new risks.

Analyst Insight

Review the executive compensation details and director nominations to assess alignment with shareholder interests and company performance.

Key Numbers

- 2023-12-31 — Fiscal Year End (Avient Corp's fiscal year end)

- 2024-03-27 — Filing Date (Date the DEF 14A was filed)

- 2024-05-16 — Period of Report End Date (The period covered by the proxy statement)

Key Players & Entities

- AVIENT CORP (company) — Registrant

- DEF 14A (filing) — Form Type

- 2024-03-27T00:00:00.000Z (date) — Filing Date

- 2024-05-16 (date) — Period of Report

- POLYONE CORP (company) — Former Company Name

- Robert M. Patterson (person) — Member of the Board

- Dr. Ashish Khandpur (person) — Member of the Board

FAQ

When did AVIENT CORP file this DEF 14A?

AVIENT CORP filed this Proxy Statement (DEF 14A) with the SEC on March 27, 2024.

What is a DEF 14A filing?

A DEF 14A is a definitive proxy statement sent to shareholders before annual meetings, covering executive compensation, board nominations, and shareholder votes. This particular DEF 14A was filed by AVIENT CORP (AVNT).

Where can I read the original DEF 14A filing from AVIENT CORP?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by AVIENT CORP.

What are the key takeaways from AVIENT CORP's DEF 14A?

AVIENT CORP filed this DEF 14A on March 27, 2024. Key takeaways: Avient Corp filed a Definitive Proxy Statement (DEF 14A) on March 27, 2024.. The filing covers the period ending May 16, 2024.. The company's fiscal year ends on December 31..

Is AVIENT CORP a risky investment based on this filing?

Based on this DEF 14A, AVIENT CORP presents a relatively low-risk profile. The filing is a routine DEF 14A, indicating standard corporate governance and shareholder communication processes rather than immediate financial distress or significant new risks.

What should investors do after reading AVIENT CORP's DEF 14A?

Review the executive compensation details and director nominations to assess alignment with shareholder interests and company performance. The overall sentiment from this filing is neutral.

How does AVIENT CORP compare to its industry peers?

Avient Corp operates in the plastics and materials industry, specifically focusing on specialty polymer formulations, colorants, and additives.

Are there regulatory concerns for AVIENT CORP?

The filing is made under the Securities Exchange Act of 1934, specifically Rule 14a-101, which governs the content of proxy statements.

Industry Context

Avient Corp operates in the plastics and materials industry, specifically focusing on specialty polymer formulations, colorants, and additives.

Regulatory Implications

The filing is made under the Securities Exchange Act of 1934, specifically Rule 14a-101, which governs the content of proxy statements.

What Investors Should Do

- Analyze the proposed director nominees and their qualifications.

- Review the details of the executive compensation packages, including base salary, bonuses, and equity awards.

- Understand the voting items and cast votes accordingly.

Key Dates

- 2024-03-27: Filing of DEF 14A — Indicates the company is providing formal proxy materials to shareholders.

- 2024-05-16: Period of Report End — Marks the end of the reporting period for which the proxy statement provides information.

Year-Over-Year Comparison

This is a DEF 14A filing, which is a standard annual disclosure for public companies regarding shareholder meetings and corporate governance.

Filing Stats: 4,487 words · 18 min read · ~15 pages · Grade level 14.9 · Accepted 2024-03-27 07:49:17

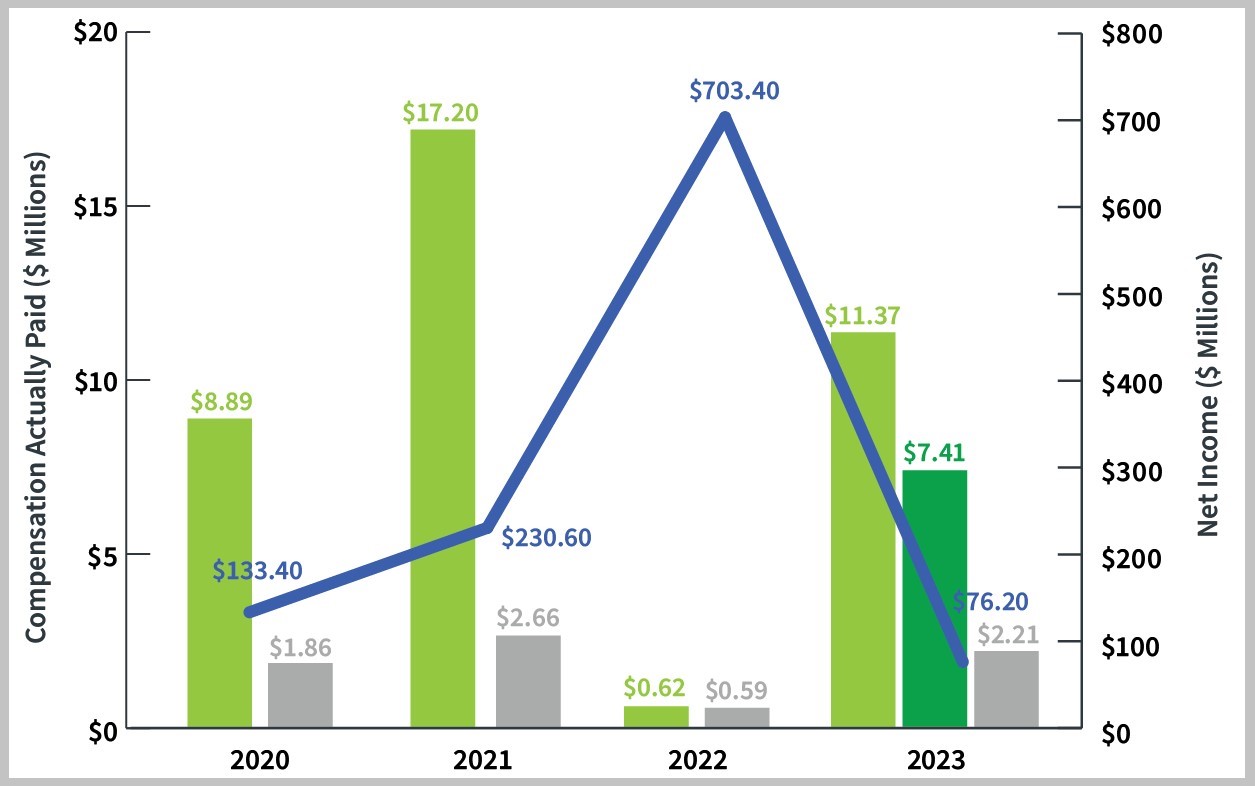

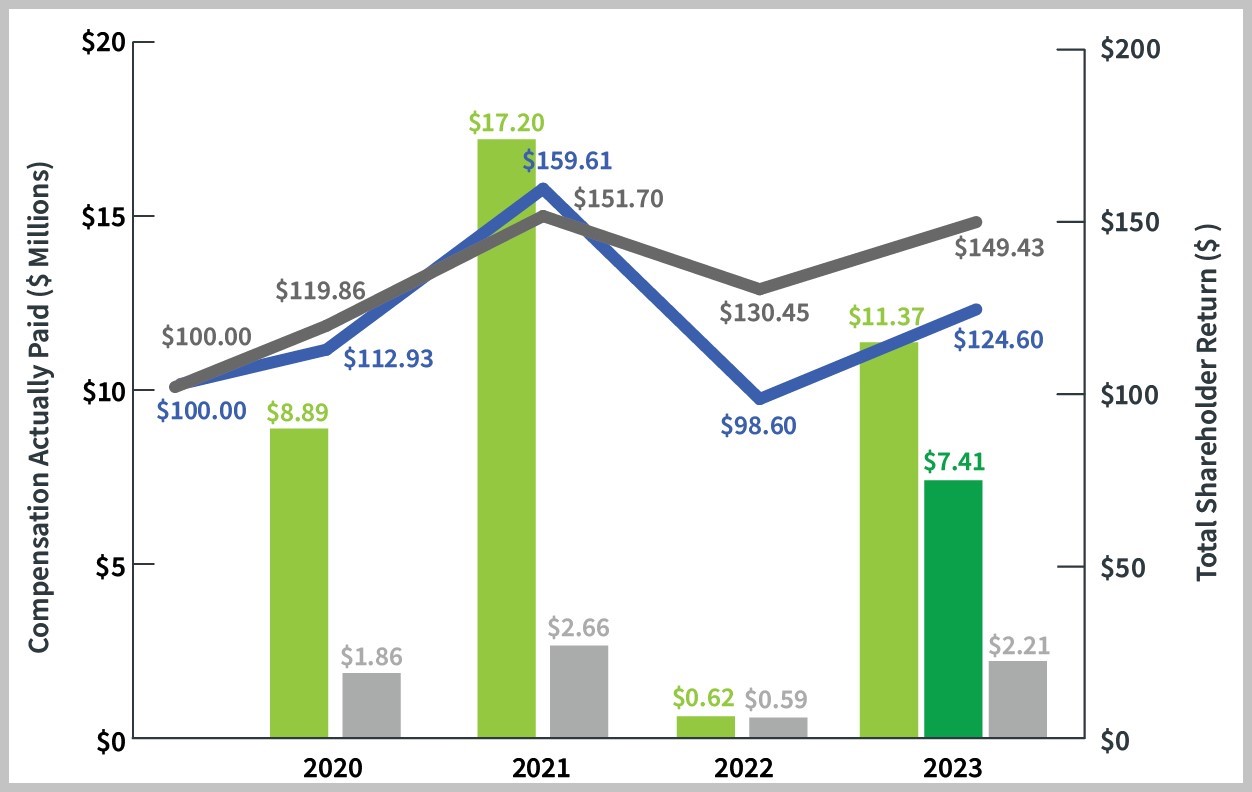

Key Financial Figures

- $0.83 — year GAAP earnings per share ("EPS") of $0.83 in 2023, compared to $0.90 from continu

- $0.90 — e ("EPS") of $0.83 in 2023, compared to $0.90 from continuing operations in 2022; Ad

- $2.36 — ng operations in 2022; Adjusted EPS of $2.36 in 2023, compared to pro forma adjusted

- $3.04 — , compared to pro forma adjusted EPS of $3.04 in 2022 (1) ; 2023 cash flow from oper

- $202 million — ) ; 2023 cash flow from operations was $202 million; excluding $104 million of taxes paid o

- $104 million — operations was $202 million; excluding $104 million of taxes paid on the sale of our Distri

- $306 million — in 2022), cash flow from operations was $306 million (1) ; Increased our dividend on an ann

- $1.03 — ividend on an annualized basis by 4% to $1.03; the 13th consecutive year of annual in

Filing Documents

- avnt-20240326.htm (DEF 14A) — 1553KB

- avnt-20240326_g1.jpg (GRAPHIC) — 31KB

- avnt-20240326_g10.jpg (GRAPHIC) — 16KB

- avnt-20240326_g11.jpg (GRAPHIC) — 16KB

- avnt-20240326_g12.jpg (GRAPHIC) — 44KB

- avnt-20240326_g13.jpg (GRAPHIC) — 118KB

- avnt-20240326_g14.jpg (GRAPHIC) — 17KB

- avnt-20240326_g15.jpg (GRAPHIC) — 69KB

- avnt-20240326_g16.jpg (GRAPHIC) — 8KB

- avnt-20240326_g17.jpg (GRAPHIC) — 14KB

- avnt-20240326_g18.jpg (GRAPHIC) — 15KB

- avnt-20240326_g19.jpg (GRAPHIC) — 16KB

- avnt-20240326_g2.jpg (GRAPHIC) — 121KB

- avnt-20240326_g20.jpg (GRAPHIC) — 68KB

- avnt-20240326_g21.jpg (GRAPHIC) — 44KB

- avnt-20240326_g22.jpg (GRAPHIC) — 7KB

- avnt-20240326_g23.jpg (GRAPHIC) — 7KB

- avnt-20240326_g24.jpg (GRAPHIC) — 8KB

- avnt-20240326_g25.jpg (GRAPHIC) — 67KB

- avnt-20240326_g26.jpg (GRAPHIC) — 21KB

- avnt-20240326_g27.jpg (GRAPHIC) — 258KB

- avnt-20240326_g28.jpg (GRAPHIC) — 197KB

- avnt-20240326_g29.jpg (GRAPHIC) — 241KB

- avnt-20240326_g3.jpg (GRAPHIC) — 5KB

- avnt-20240326_g30.jpg (GRAPHIC) — 55KB

- avnt-20240326_g31.jpg (GRAPHIC) — 237KB

- avnt-20240326_g32.jpg (GRAPHIC) — 253KB

- avnt-20240326_g33.jpg (GRAPHIC) — 231KB

- avnt-20240326_g34.jpg (GRAPHIC) — 162KB

- avnt-20240326_g35.jpg (GRAPHIC) — 253KB

- avnt-20240326_g36.jpg (GRAPHIC) — 193KB

- avnt-20240326_g37.jpg (GRAPHIC) — 73KB

- avnt-20240326_g38.jpg (GRAPHIC) — 212KB

- avnt-20240326_g39.jpg (GRAPHIC) — 141KB

- avnt-20240326_g4.jpg (GRAPHIC) — 184KB

- avnt-20240326_g40.jpg (GRAPHIC) — 61KB

- avnt-20240326_g41.jpg (GRAPHIC) — 101KB

- avnt-20240326_g42.jpg (GRAPHIC) — 104KB

- avnt-20240326_g43.jpg (GRAPHIC) — 95KB

- avnt-20240326_g44.jpg (GRAPHIC) — 134KB

- avnt-20240326_g45.jpg (GRAPHIC) — 149KB

- avnt-20240326_g5.jpg (GRAPHIC) — 179KB

- avnt-20240326_g6.jpg (GRAPHIC) — 1KB

- avnt-20240326_g7.jpg (GRAPHIC) — 1KB

- avnt-20240326_g8.jpg (GRAPHIC) — 1KB

- avnt-20240326_g9.jpg (GRAPHIC) — 67KB

- 0001122976-24-000025.txt ( ) — 13520KB

- avnt-20240326.xsd (EX-101.SCH) — 4KB

- avnt-20240326_def.xml (EX-101.DEF) — 6KB

- avnt-20240326_lab.xml (EX-101.LAB) — 8KB

- avnt-20240326_pre.xml (EX-101.PRE) — 5KB

- avnt-20240326_htm.xml (XML) — 116KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Executive Compensation Philosophy and Objectives 46

Executive Compensation Philosophy and Objectives 46 What We Pay and Why: Elements of Compensation 48 Other Aspects of our Compensation Programs 54

Executive Compensation

Executive Compensation 59 2023 Summary Compensation Table 59 2023 Grants of Plan-Based Awards 62 Outstanding Equity Awards at 2023 Fiscal Year-End 64 2023 Option Exercises and Stock Vested 65 2023 Non Qualified Deferred Compensation 65 Potential Payments Upon Termination or Change of Control 66 CEO Pay Ratio Disclosure 71 Pay Versus Performance Disclosure 72 Compensation Committee Interlocks and Insider Participation 75 Risk Assessment of the Compensation Programs 75 Compensation Committee Report 76 Miscellaneous Provisions 77 Internet Availability of Proxy Materials 77 Voting at the Meeting 77 Revoking a Proxy 78 Shareholder Proposals 78 Proxy Solicitation 79 Householding of Proxy Materials 79 Appendix A A-1 In this proxy statement, statements that are not reported financial results or other historical information are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements give current expectations or forecasts of future events and are not guarantees of future performance. They are based on management's expectations that involve a number of business risks and uncertainties, any of which could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. You can identify these statements by the fact that they do not relate strictly to historic or current facts. They use words such as "will," "anticipate," "estimate," "expect," "project," "intend," "plan," "believe" and other words and terms of similar meaning in connection with any discussion of future operating or financial condition, performance and/or sales. Factors that could cause our actual results to differ materially from those implied by forward-looking statements include, but are not limited to, our ability to successfully achieve our sustainability goals within the expected time frames or at all, and those other factors described in detail in Part l o