Eastman Kodak Co. Files Definitive Proxy Statement for 2024 Annual Meeting

Ticker: KODK · Form: DEF 14A · Filed: Apr 5, 2024 · CIK: 31235

Sentiment: neutral

Topics: Proxy Statement, Annual Meeting, Corporate Governance, Executive Compensation, Director Election

TL;DR

<b>Eastman Kodak Co. has filed its definitive proxy statement for the 2024 Annual Meeting, detailing director elections, corporate governance, and executive compensation.</b>

AI Summary

EASTMAN KODAK CO (KODK) filed a Proxy Statement (DEF 14A) with the SEC on April 5, 2024. Eastman Kodak Company filed its Definitive Proxy Statement (DEF 14A) on April 5, 2024. The filing concerns the Notice of the 2024 Annual Meeting of Shareholders. Key topics include the election of directors and corporate governance. Executive compensation details and reports from board committees are also included. Shareholders will receive a printed copy of the 2023 Annual Report on Form 10-K.

Why It Matters

For investors and stakeholders tracking EASTMAN KODAK CO, this filing contains several important signals. This filing provides shareholders with crucial information regarding the company's leadership, governance practices, and executive pay structure ahead of the annual meeting. Shareholders can review proposals, director nominees, and compensation details to make informed voting decisions.

Risk Assessment

Risk Level: — EASTMAN KODAK CO shows moderate risk based on this filing. The filing is a routine proxy statement, providing information to shareholders rather than announcing new material events, thus posing low risk.

Analyst Insight

Shareholders should review the director nominees and executive compensation details to prepare for the upcoming annual meeting and cast informed votes.

Key Numbers

- 2024 — Annual Meeting Year (Notice of 2024 Annual Meeting)

- 2023 — Annual Report Year (Printed Copy of 2023 Annual Report on Form 10-K)

Key Players & Entities

- EASTMAN KODAK CO (company) — Registrant

- DEF 14A (filing) — Form Type

- 2024 Annual Meeting (event) — Meeting Date

- April 5, 2024 (date) — Filing Date

- Rochester, New York (location) — Business Address

- 343 State St (address) — Business Address

FAQ

When did EASTMAN KODAK CO file this DEF 14A?

EASTMAN KODAK CO filed this Proxy Statement (DEF 14A) with the SEC on April 5, 2024.

What is a DEF 14A filing?

A DEF 14A is a definitive proxy statement sent to shareholders before annual meetings, covering executive compensation, board nominations, and shareholder votes. This particular DEF 14A was filed by EASTMAN KODAK CO (KODK).

Where can I read the original DEF 14A filing from EASTMAN KODAK CO?

You can access the original filing directly on the SEC's EDGAR system. The filing is publicly available and includes all exhibits and attachments submitted by EASTMAN KODAK CO.

What are the key takeaways from EASTMAN KODAK CO's DEF 14A?

EASTMAN KODAK CO filed this DEF 14A on April 5, 2024. Key takeaways: Eastman Kodak Company filed its Definitive Proxy Statement (DEF 14A) on April 5, 2024.. The filing concerns the Notice of the 2024 Annual Meeting of Shareholders.. Key topics include the election of directors and corporate governance..

Is EASTMAN KODAK CO a risky investment based on this filing?

Based on this DEF 14A, EASTMAN KODAK CO presents a moderate-risk profile. The filing is a routine proxy statement, providing information to shareholders rather than announcing new material events, thus posing low risk.

What should investors do after reading EASTMAN KODAK CO's DEF 14A?

Shareholders should review the director nominees and executive compensation details to prepare for the upcoming annual meeting and cast informed votes. The overall sentiment from this filing is neutral.

How does EASTMAN KODAK CO compare to its industry peers?

Eastman Kodak operates in the photographic equipment and supplies industry, historically known for its film products.

Are there regulatory concerns for EASTMAN KODAK CO?

The filing is made under Section 14(a) of the Securities Exchange Act of 1934, governing proxy solicitations.

Industry Context

Eastman Kodak operates in the photographic equipment and supplies industry, historically known for its film products.

Regulatory Implications

The filing is made under Section 14(a) of the Securities Exchange Act of 1934, governing proxy solicitations.

What Investors Should Do

- Review the list of director nominees and their qualifications.

- Examine the executive compensation details and the rationale behind them.

- Understand the proposals to be voted on at the 2024 Annual Meeting.

Key Dates

- 2024-04-05: Filing Date — Filing of Definitive Proxy Statement

Year-Over-Year Comparison

This is the initial filing of the 2024 proxy statement, providing forward-looking information for the upcoming annual meeting.

Filing Stats: 4,792 words · 19 min read · ~16 pages · Grade level 10.6 · Accepted 2024-04-05 08:01:27

Filing Documents

- ny20023461x1_def14a.htm (DEF 14A) — 1630KB

- logo_kodax.jpg (GRAPHIC) — 15KB

- sig_rbyrd.jpg (GRAPHIC) — 12KB

- sig_rbyrdx1.jpg (GRAPHIC) — 13KB

- ny20023461x1_pc01.jpg (GRAPHIC) — 557KB

- ny20023461x1_pc02.jpg (GRAPHIC) — 577KB

- ny20023461x1_pvpchart01x1.jpg (GRAPHIC) — 140KB

- ny20023461x1_pvpchart02x1.jpg (GRAPHIC) — 117KB

- sig_jcontinenza.jpg (GRAPHIC) — 15KB

- 0001140361-24-018157.txt ( ) — 6083KB

- kodk-20240515.xsd (EX-101.SCH) — 5KB

- kodk-20240515_def.xml (EX-101.DEF) — 7KB

- kodk-20240515_lab.xml (EX-101.LAB) — 14KB

- kodk-20240515_pre.xml (EX-101.PRE) — 6KB

- ny20023461x1_def14a_htm.xml (XML) — 155KB

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

EXECUTIVE COMPENSATION

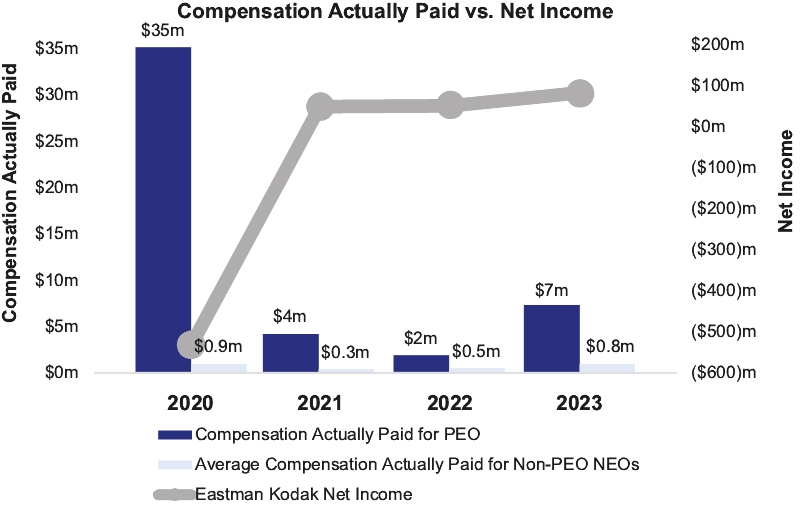

EXECUTIVE COMPENSATION Report of the Compensation, Nominating and Governance Committee 19 Compensation Discussion and Analysis 19 Executive Summary 19 Determining Executive Compensation 20 Elements of Compensation 22 2023 Compensation Decisions 22 Other Compensation 24 Program Governance 26 Compensation of Named Executive Officers 28 Summary Compensation Table 28 Employment Agreements 30 Grants of Plan-Based Awards Table 31 Outstanding Equity Awards at 2023 Fiscal Year-End Table 32 Option Exercises and Stock Vested Table 34 Pension Benefits for 2023 34 Pension Benefits Table 35 Non-Qualified Deferred Compensation 37 Potential Payments upon Termination or Change in Control 37 Severance Payments Table 40 CEO Pay Ratio 42 Pay Versus Performance 43 DIRECTOR COMPENSATION Director Compensation 46 PROPOSAL 2 Proposal 2 - Advisory Vote to Approve the Compensation of our Named Executive Officers 48

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT Beneficial Security Ownership of More Than 5% of the Company's Shares 49 Beneficial Security Ownership of Directors, Nominees and Executive Officers 51 DELINQUENT SECTION 16(A) REPORTS 52 CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS 52 PROPOSAL 3 Proposal 3 – Approval of the Second Amendment to the Amended and Restated 2013 Omnibus Incentive Plan 55 PRINCIPAL ACCOUNTING FEES AND SERVICES 62 Audit and Non-Audit Fees 62 Policy Regarding Pre-Approval of Services Provided by our Independent Accountants 62 PROPOSAL 4 63 Proposal 4 – Ratification of the Audit and Finance Committee's Selection of Ernst & Young LLP as our Independent Registered Public Accounting Firm 63 TABLE OF CONTENTS CAUTIONARY NOTE: This proxy statement includes "forward–looking statements" as that term is defined under the Private Securities Litigation Reform Act of 1995. Forward–looking statements include statements concerning Eastman Kodak Company's plans, objectives, goals, strategies, future events, and business trends and other information that is not historical information. When used in this document, the words "estimate," "expect," "intend," "believe," "continue," "goals," "target," "seek," "ongoing," or future or conditional verbs, such as "will," "should," "could," or "may," and similar words and expressions, as well as statements that do not relate strictly to historical or current facts, are intended to identify forward–looking statements. All forward–looking statements are based upon our current expectations and assumptions. Forward-looking statements are subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or those expressed in or implied by such forward-looking statements. Important factors that could cause actual events or results to differ materially from the forward-looking statements include, among others, the